In April 2026, South Korea posted $85.9 billion in goods exports, a 48 percent surge from a year earlier, with semiconductors exceeding $30 billion for the second consecutive month. Semiconductors, EV batteries, advanced displays: the industries at the core of South Korea’s export economy are running at full tilt. But those figures hide a more concerning upstream reality: a narrow set of critical minerals, most still sourced overwhelmingly from China, makes all of it possible.

Trade data from South Korea’s mineral import statistics system, KOMIS, now covering all of 2025, offers the clearest picture yet of where South Korea’s critical mineral supply chains have strengthened and where they remain exposed. The picture is not a simple success story or a simple failure. It is a bifurcated landscape: real progress in some places, deepening concentration in others. The most significant diversification came after Beijing imposed controls on a mineral first.

The problem is not South Korea’s alone. Because Korean batteries, displays, and semiconductors feed into U.S. and allied supply chains, China’s leverage over these inputs is also an allied economic security vulnerability.

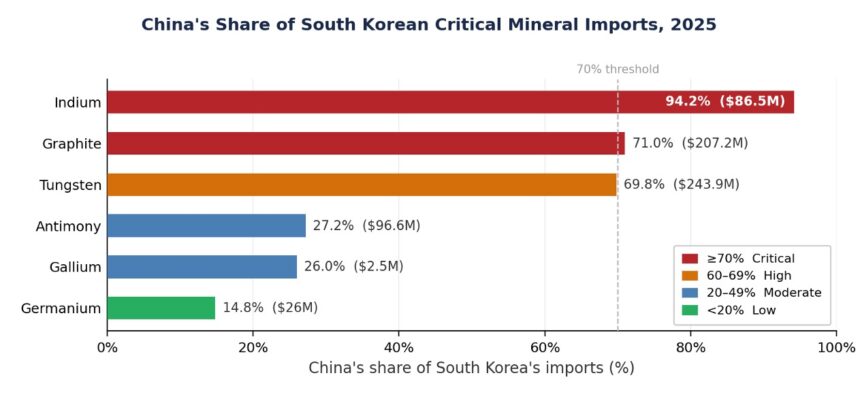

For six minerals critical to South Korea’s most strategically important industries, China’s 2025 share of Korean imports ranges from 14.8 percent to 94.2 percent (see Figure 1 below). Germanium, used in infrared optics and fiber optic cable, sits at the low end. Indium — the element that helps flat-panel displays and touchscreens conduct electricity while staying transparent — sits at the high end, with 94.2 percent of South Korean imports coming from China.

Figure 1: China’s share of South Korean critical mineral imports, 2025. Dollar values in parentheses are total 2025 South Korean import values, not China-origin only. Source: Author’s calculations based on KOMIS annual mineral trade statistics (komis.or.kr).

Citing the Korea Institute of Geoscience and Mineral Resources, a CSIS analysis noted that South Korea’s net import reliance on critical minerals exceeds 99.7 percent. For South Korea, then, the question is not whether to import; it is from whom, under what terms, and what options exist when that supply is disrupted.

With that in mind, the most striking feature of the KOMIS data is not the persistence of Chinese dominance but how quickly South Korean sourcing shifted away from China after Beijing imposed export controls.

Gallium is the clearest case. After China announced export controls on gallium and germanium in August 2023, South Korean buyers initially front-loaded purchases: China’s share of Korean gallium imports actually rose to 73.6 percent in 2024 as firms stockpiled ahead of tighter restrictions. By 2025, the rebalancing was dramatic. China’s share fell to 26.0 percent, with Germany (25.9 percent), the United States (24.3 percent) and Japan (18.2 percent) filling in the gap roughly equally. The shift, accomplished in roughly 18 months, accelerated sharply after the export control announcement.

Germanium diversified more durably and more completely. Canada now accounts for 70.7 percent of South Korea’s germanium imports, with China supplying just 14.8 percent, down from 59.3 percent in 2023. Available processing capacity in Canada helped make the transition possible.

The September 2024 Chinese export controls on antimony coincided with a similar sourcing shift. China’s share of South Korean antimony imports fell from 69.0 percent in 2024 to 27.2 percent in 2025, with Thailand emerging as the new primary supplier at 48.6 percent. The timing suggests export controls acted as a catalyst.

Figure 2: China’s share of South Korean gallium, germanium, and antimony imports, 2019–2025. Dotted lines mark Chinese export control announcement dates. Source: Author’s calculations based on KOMIS annual mineral trade statistics (komis.or.kr).

The antimony numbers require scrutiny that import level data cannot provide.

China remains the dominant producer and refiner of antimony globally, but it is also a net importer of antimony concentrates and depends on ore from countries including Thailand, Myanmar, and Russia. As a result, South Korean customs data showing a rise in Thailand-sourced antimony may not reflect genuinely independent upstream sourcing. The geographic shift visible in KOMIS figures may represent a change in country of last processing, not in upstream origin.

Until smelter-level provenance can be verified, Seoul should treat the apparent diversification with caution. A falling Chinese share in import data does not, by itself, confirm reduced strategic exposure.

The broader lesson is clear: a supply chain is not secure simply because the final shipment originates outside China.

Where gallium and germanium have diversified following Beijing’s export controls, three other minerals show the opposite trajectory.

Figure 3: China’s share of South Korean indium, graphite, and tungsten imports, 2015 vs. 2025. Arrows show direction of change over the decade. Dollar values shown are total 2025 South Korean import values, not China-origin imports. Source: Author’s calculations based on KOMIS annual mineral trade statistics (komis.or.kr).

China’s share of South Korea’s indium imports has risen from 44.1 percent in 2015 to 94.2 percent in 2025, moving in precisely the wrong direction over a decade of official critical minerals policy. South Korea imported $86.5 million of indium in 2025. That modest figure nonetheless represents a single-source dependency for an element that is difficult to substitute in display manufacturing and certain semiconductor applications. Japan accounts for 3.6 percent of South Korea’s supply; no other country reaches 2 percent.

The structural constraint cannot be resolved within any near-term policy window. Indium is not typically mined on its own. According to the USGS Mineral Commodity Summaries, it is most commonly recovered from sphalerite, a zinc-sulfide ore mineral, while recovery from most other base-metal sulfide deposits is not economic. China is also the leading global producer of indium, accounting for roughly 70 percent of world production. The supply picture therefore cannot be changed simply by outreach missions or non-binding memoranda of understanding.

Graphite presents a similar case, at a larger scale. China’s share of South Korean graphite imports has risen from 52.4 percent in 2015 to 71.0 percent in 2025, at $207.2 million annually. For South Korea’s battery producers, the vulnerability lies not only in graphite supply but in the processing capacity needed to convert it into battery-ready anode material. Alternative mining and processing projects outside China are developing, but not yet at the scale needed to quickly offset Chinese supply.

Tungsten rounds out the structural exposure picture. China supplied 69.8 percent of South Korea’s tungsten imports in 2025, worth about $170.2 million out of roughly $243.9 million in total annual imports – just below the 70 percent high-reliance benchmark used in this analysis. The risk is not only concentration, but substitution: tungsten is used in cemented carbide parts, specialty steels, and electronic components, and replacing it can raise costs or reduce performance.

The chain of dependencies runs beyond Korean borders. South Korean battery makers supply U.S. automakers. South Korean display manufacturers supply U.S. electronics brands and defense electronics supply chains. Korean foundry and semiconductor packaging capacity complements Taiwan’s in ways that U.S. industrial planners now treat as strategically significant. A Chinese restriction on graphite or indium would not stay contained within South Korean industry; it would cascade into allied semiconductor and battery production, and current strategic stockpiling levels would offer only a partial buffer.

South Korea chaired the Minerals Security Partnership (MSP) starting in July 2024. In February 2026, the U.S. State Department announced FORGE (Forum on Resource Geostrategic Engagement) as the MSP’s successor initiative, with South Korea continuing as chair through June 2026. That platform is a time-limited opportunity to set the agenda for what allied mineral cooperation does next.

The import patterns visible in KOMIS data through 2025 show why South Korea needs differentiated policy, not a uniform diversification target.

South Korea’s government has set a goal of reducing overall import concentration from approximately 80 percent to 50 percent by 2030. An analysis published in February 2026 by the Korea Institute for International Economic Policy (KIEP) found that South Korea’s current toolkit — bilateral MOUs with resource-rich countries, existing FTAs, and public stockpiling programs — lacks the enforceable architecture to deliver supply security when it is actually tested.

MOUs are declarations, not binding commitments. They cannot prevent export restrictions, protect investments, or move technical personnel across borders when a mine or processing facility needs them. The KIEP brief proposed three priority pillars for enforceable “mini-deals”: disciplines on export-restrictive measures; investment and investor protections; and technical workforce mobility arrangements. The number of export-restriction measures on industrial raw materials globally has risen from 193 in 2009 to 507 in 2023. Non-binding cooperation instruments have not kept pace.

For the minerals where diversification has already happened – like gallium and germanium – the immediate priority is locking in those gains. That means converting current supplier relationships with Canada, Germany, and the United States into long-term offtake agreements with enforceable terms before lower-cost Chinese supply resumes and alternative producers lose market share. Allied country producers need contractual frameworks that make their capacity economically viable over a long horizon, not just during Chinese restrictions.

For the minerals where diversification cannot happen quickly – indium, graphite, tungsten – the appropriate response is strategic stockpiling. South Korea’s stockpiling targets were raised to 100 days in 2023 from 54 days, a meaningful improvement. But stockpile coverage varies by mineral, and indium in particular has been underrepresented in national reserve programs relative to its industrial importance. Coordinating reserve levels with U.S. and Japanese partners through FORGE would reduce acute vulnerability if Beijing restricts supply.

On antimony, and on other minerals where country-of-last-processing data may not reflect actual upstream origin, Seoul should press for FORGE-level traceability standards. Supply chain verification that reaches the smelter level, not just the border, is what meaningful diversification requires. South Korea’s chairmanship gives it standing to push that standard into FORGE’s project evaluation criteria.

The KOMIS data through 2025 gives South Korea a clearer picture of where its mineral supply chains are resilient and where they remain exposed. Diversification has followed Beijing’s export controls where alternative capacity existed. It has not happened, and will not happen quickly, for indium, graphite and tungsten, the minerals embedded deepest in South Korea’s highest-value export industries.

South Korea’s strength in semiconductors and batteries is real. So is the upstream vulnerability that underpins them. Closing the gap between those two facts is the defining supply chain challenge of the decade. As its FORGE chairmanship nears its end in June 2026, Seoul still has a narrow window to push that agenda.