With the inventory market not too long ago hitting new all-time highs once more, instances are thrilling for people who find themselves absolutely invested, however these circumstances could be extra irritating for individuals who have money obtainable to place to work. Increased inventory costs do make it a bit more durable for cut price hunters to search out offers, however shares do not all rise or fall on a synchronized schedule. Some invariably lag behind these broad-market patterns.

The powerful a part of looking for out bargains amongst these laggard shares is that there is normally an excellent purpose why an organization’s shares did not take part within the rally. Nonetheless, even when there is a good purpose, on the proper costs, out-of-favor shares could be value shopping for.

With that in thoughts, three Motley Idiot contributors went in search of shares the latest bull market has left behind that may have a little bit of life forward of them, regardless of Wall Road’s pessimism. They got here up with Pfizer (NYSE: PFE), Confluent (NASDAQ: CFLT), and Kinder Morgan (NYSE: KMI). However solely you possibly can determine whether or not they’re low-cost sufficient to be value a spot in your portfolio.

A mighty drug maker introduced low by the market

Eric Volkman (Pfizer): With uncommon exceptions, star energy hardly ever lasts perpetually. One instance of an organization that not too long ago skilled the draw back of this dynamic is pharmaceutical big Pfizer.

A number of years in the past, Pfizer was a scorching merchandise because of its heavy involvement within the struggle in opposition to COVID-19. It was the co-developer of the go-to coronavirus vaccine Comirnaty. On prime of that, it’s the firm behind the well-known COVID antiviral therapy Paxlovid.

Within the thick of the pandemic, when a whole lot of tens of millions of individuals have been desirous to get inoculated, and when therapies for the illness have been in excessive demand, Pfizer skilled huge leaps in income and profitability.

Even the mightiest firm would discover it difficult to comply with up that kind of efficiency with an analogous second act, and Pfizer is falling quick within the minds of many. In any case, each its not too long ago launched fourth-quarter and full-year 2023 headline figures have been down considerably because the pandemic has advanced into an endemic and the general public well being disaster has receded. Income for This autumn and the complete 12 months fell by greater than 40% on a year-over-year foundation, with non-GAAP (adjusted) internet earnings nose-diving by 91% within the quarter.

But these fourth-quarter figures beat the collective estimates from analysts, who have been anticipating the pharmaceutical big to submit a reasonably deep adjusted internet loss. A lot of the upside shock was resulting from Comirnaty, which remains to be making its means into the arms of people who find themselves conscious that COVID-19 stays a menace.

Nevertheless, gross sales of a number of of Pfizer’s prime merchandise fell, compounding the widely bearish response to the earnings report. For instance, within the face of intensifying competitors, most cancers therapy Ibrance noticed an almost 13% year-over-year decline in gross sales. Looming patent expirations for Ibrance and different prime sellers are additionally making buyers fret.

They actually should not. Pfizer nonetheless has a strong lineup of blockbuster medication, and it has a strong pipeline with potential blockbusters in improvement.

In the meantime, its valuations look sickly, and can certainly enhance as soon as the market will get previous the concept the corporate cannot sufficiently recuperate from the decline in its COVID-related revenues.

Its ahead P/E is barely over 12, and its trailing price-to-sales ratio is a feeble 2.3. I do not suppose it’s going to proceed to commerce at such cut price ranges for lengthy. Strengthening the purchase case is the corporate’s dividend, some of the regular and dependable within the healthcare sector. On the present share value, it yields greater than 6% — sky-high for a as soon as and future blue chip inventory.

Do not name it a comeback

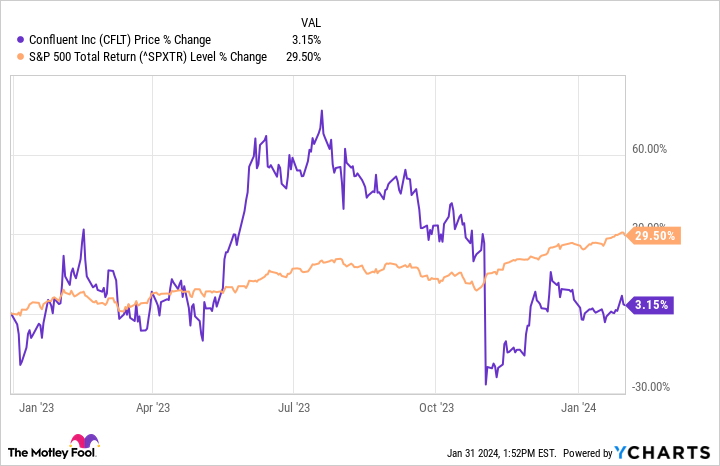

Jason Corridor (Confluent): One have a look at the chart beneath could make buyers suppose that Confluent is in bother.

From its early 2023 low to its excessive level, Confluent’s inventory value doubled, however then headed decrease once more earlier than tumbling sharply again previous that prior low when it reported third-quarter leads to November.

What despatched its shares tumbling? Frankly, the standard volatility of being a youthful, still-developing enterprise. Confluent is a pacesetter in knowledge streaming, and buyers are targeted on its progress charges and buyer enlargement. When it reported some churn with a number of huge clients that will carry over into early 2024, the market form of freaked out.

My evaluation says this was an overreaction. Confluent’s progress story stays intact.

Income was up 32% within the third quarter, and Confluent Cloud income was up 61%. Its progress has slowed, and buyers count on to listen to that it slowed additional to 22% and 43% within the fourth quarter. (The corporate will report outcomes for that interval on Wednesday.) However Confluent Cloud (its model of Kafka constructed to dwell in AWS, Azure, and so on) remains to be anticipated to develop by greater than 40% per 12 months.

Buyer progress remains to be within the high-teens percentages, and the variety of clients spending $100,000 or extra with it yearly is rising even sooner. In consequence, margins are enhancing and money flows are getting stronger. The corporate forecast that it will be free-cash-flow breakeven within the fourth quarter, and expects to start out producing constructive free money movement in 2024.

So whereas the market sees danger, I see an organization that is getting stronger and safer with every passing quarter. Now’s the time to purchase this upstart within the courageous new world of how companies handle and use knowledge.

This firm’s trade nonetheless has many years of life left in it

Chuck Saletta (Kinder Morgan): Oil and pure fuel might not be the sexiest types of vitality today, however they continue to be in sturdy demand all through the world. Certainly, based on the U.S. Vitality Info Administration’s most up-to-date Annual Vitality Outlook, oil and pure fuel use is predicted to remain roughly steady between now and 2050.

Past that, it is not too far a stretch to undertaking past 2050 and presume that even when our provides of greener vitality proceed to develop, it’s going to nonetheless take a very long time after that to fully eradicate oil and pure fuel from the world’s vitality combine. In any case, you possibly can’t actually go from about 20 million barrels of oil per day and 30 trillion cubic toes of pure fuel use per 12 months to utterly nothing in a single day.

As well as, even when you do think about a decline in oil and pure fuel use over the very lengthy haul, pipeline firms like Kinder Morgan are prone to be among the many longest-lasting elements of the trade. Pipelines have excessive up-front prices to construct, however they profit from comparatively low prices per barrel of oil or cubic foot of pure fuel to move that vitality.

In consequence, so long as oil and pure fuel are wanted and have to maneuver from the place they’re produced to the place they’re processed and consumed, pipelines will nonetheless be wanted to maneuver them round. Different transportation strategies — like vehicles and trains — will seemingly see their use for oil and pure fuel transportation drop earlier than pipelines do.

Regardless of these first rate prospects for many years to return, Kinder Morgan’s shares have principally gone nowhere for greater than 5 years, at the same time as its dividends have continued to recuperate. Its market capitalization is round $38 billion, and it generated round $5.6 billion in money from operations over the previous 12 months. At that valuation — lower than 7 instances its cash-generating capacity — the market is nearly giving up on the corporate, regardless of these strong many years seemingly forward of it.

Kinder Morgan might not be the fastest-growing firm on the planet, however given its prospects, its shares definitely look low-cost sufficient to be value contemplating in the meanwhile.

Get began now

Though the market does often depart strong firms behind when it rallies, true bargains hardly ever stay bargains for lengthy. That is why now’s the time to have a look for your self and see when you suppose these companies’ shares are value selecting up at their present costs. Even when the market does not find yourself bidding them up for giant rallies, you simply may end up with shares of high quality firms you may be happy to carry onto for a few years to return.

Do you have to make investments $1,000 in Pfizer proper now?

Before you purchase inventory in Pfizer, think about this:

The Motley Idiot Inventory Advisor analyst crew simply recognized what they imagine are the 10 best stocks for buyers to purchase now… and Pfizer wasn’t one in all them. The ten shares that made the minimize may produce monster returns within the coming years.

Inventory Advisor offers buyers with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than tripled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of January 29, 2024

Chuck Saletta has positions in Kinder Morgan and Pfizer and has the next choices: lengthy January 2026 $25 calls on Pfizer, quick January 2026 $25 places on Pfizer, quick March 2024 $22.50 places on Pfizer, and quick March 2024 $27.50 calls on Pfizer. Eric Volkman has no place in any of the shares talked about. Jason Hall has positions in Confluent. The Motley Idiot has positions in and recommends Confluent, Kinder Morgan, and Pfizer. The Motley Idiot has a disclosure policy.

The Bull Market Left These 3 Stocks Behind, but They’re Buys Right Now was initially revealed by The Motley Idiot