Scorching off the approval of its gene remedy for a pair of uncommon hereditary blood issues, Vertex Prescription drugs (NASDAQ: VRTX) will quickly have one other remedy up for approval, and the monetary implications are huge. However they don’t seem to be huge simply because it stands to crank out billions in extra income. As a substitute, the plan is to shell out the equal of $100 million in order that the potential new drug can compete for the market share of certainly one of its already commercialized medicines as quickly as doable.

What is going on on right here? It is time to dig in and determine it out in order that buyers can determine what to do.

Is that this excellent news truly unhealthy information for shareholders?

Per the outcomes of a section 3 scientific trial reported Feb. 5, Vertex’s newest candidate for treating cystic fibrosis (CF), a uncommon and critical genetic illness of the lung, is each secure and efficient. The drugs is presently referred to as “vanza triple” as a result of it combines the molecule vanzacaftor and two different medication. One of many three compounds, tezacaftor, is already in one of many firm’s medicines available on the market, although the others aren’t.

Within the scientific trial, the vanza triple combo carried out at the least in addition to Trikafta, the biopharma’s best-selling product for CF. By one metric — how a lot the remedy decreased the extent of detectable chloride in sufferers’ sweat — the combo was superior, and its facet impact burden comparable. That poses an fascinating drawback.

In 2023, Trikafta was chargeable for roughly $9 billion in gross sales from a high line of roughly $10 billion. If the brand new medication will get approval from regulators on the Meals and Drug Administration (FDA), which administration plans to petition for by mid-2024, Vertex can have two merchandise in direct competitors with one another available on the market concurrently. There may be possible not any alternative for sufferers to take each therapies directly, and it’s unclear whether or not there’s a probability that a big group of sufferers will reply higher to the older mixture than the brand new one.

Due to this fact, the likelihood of the vanza triple mixture cannibalizing Trikafta’s market share may be very excessive. Buyers might balk at any determination to proceed and go for the approval as they might relatively proceed milking income from gross sales of Trikafta for years and years, transitioning to a brand new product solely when generic rivals begin to encroach.

They usually would possibly balk even more durable on the management-endorsed concept of expending an asset value within the ballpark of $100 million to start out the cannibalization course of even quicker. The asset in query is what’s referred to as a precedence assessment voucher (PRV), which is a government-issued piece of paper that entitles the bearer to get (you guessed it) a privileged regulatory standing within the assessment levels of the drug approval course of, thereby chopping the time it takes to go from submitting the paperwork to getting a choice on commercialization by a handful of months. In current instances, many biopharmas have traded PRVs to one another, preferring to get money relatively than save time, and $100 million is the worth of a typical sale.

Buyers are more likely to marvel why administration appears to be in such a rush to torpedo the corporate’s most profitable product.

One essential element explains every thing

Vertex is not being impatient, neither is the choice to make use of the PRV a poor one. The truth is, the transfer was fastidiously calculated and can possible prove for the very best for sufferers and shareholders alike. Here is why.

Per administration, a smaller proportion of income from gross sales of the vanza triple drug can be siphoned off to pay out royalties to exterior events than with its present portfolio of CF medicines. So, by commercializing the vanza mixture, the enterprise will fatten its profit margin, even when it doesn’t dramatically enhance its income, as a result of it’ll pay fewer royalties.

Utilizing the PRV thus implies that administration sees the earnings advantage of getting the drug to market a bit quicker as being bigger than the sale value of the voucher. That perspective is all of the extra credible when taking the royalty difficulty under consideration, because it considerably adjustments the financial profit of every month the medication spends available on the market.

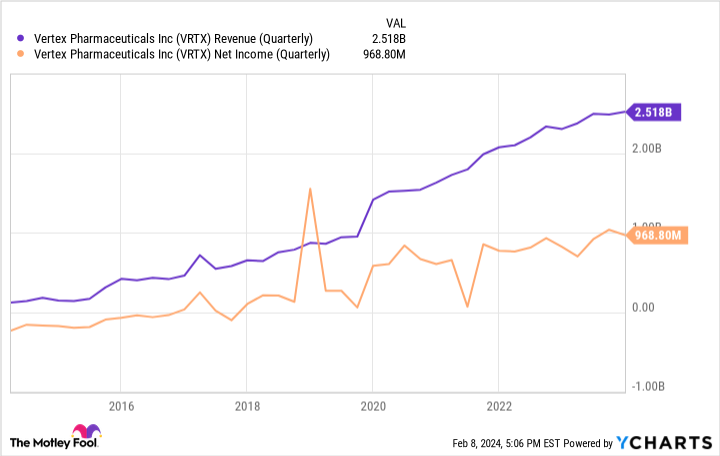

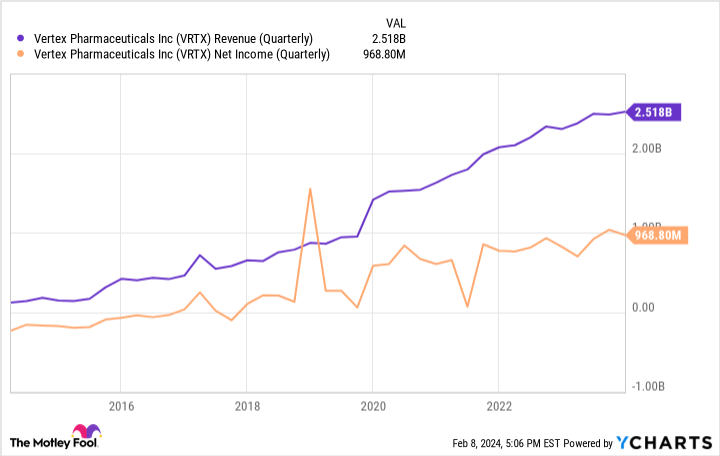

Moreover, it is essential to acknowledge that this is not Vertex’s first rodeo with regards to gracefully changing certainly one of its older merchandise with a shinier newer model that works a bit higher. If something, the corporate is an professional at cannibalizing its CF market share many times whereas nonetheless rising, having commercialized 4 completely different however overlapping medication in succession over time. Simply have a look at this chart:

As you possibly can see, the earlier shakeups of its CF merchandise did not depart shareholders within the poorhouse, and this time will not both. If something, this can be a bullish setup for the inventory. In spite of everything, it will quickly be raking in much more cash by serving the identical core market, and sufferers will get higher therapy, too.

The place to speculate $1,000 proper now

When our analyst workforce has a inventory tip, it may pay to hear. In spite of everything, the e-newsletter they’ve run for 20 years, Motley Idiot Inventory Advisor, has greater than tripled the market.*

They only revealed what they imagine are the 10 best stocks for buyers to purchase proper now… and Vertex Prescription drugs made the listing — however there are 9 different shares it’s possible you’ll be overlooking.

*Inventory Advisor returns as of February 12, 2024

Alex Carchidi has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Vertex Prescription drugs. The Motley Idiot has a disclosure policy.

Vertex Pharmaceuticals Will Use $100 Million to Tank Its Own Market Share. Here’s Why That’s a Smart Move. was initially printed by The Motley Idiot