Do you like dividends? After all you do — and rightly so!

In a latest examine carried out by Mike Wilson, Chief Funding Officer at Morgan Stanley, the evaluation targeted on the efficiency of dividend-paying shares in comparison with non-dividend-paying shares for the reason that 12 months 2000. The historic information underscores a compelling development: dividend-paying shares persistently outperform non-dividend shares over the medium to long run.

That outperformance has even been extra pronounced in occasions of uncertainty and market retreats. “Particularly,” Wilson famous, “the vast majority of outperformance comes throughout massive market pullbacks corresponding to 2000, 2008, 2015, and 2020.”

With uncertainty at present prevailing, Wilson believes it could be the fitting time to noticeably contemplate loading up on these traditional defensive performs.

Towards this backdrop, the analysts at Morgan Stanley have pinpointed a possibility in a pair of dividend stocks with attractive attributes: a excessive dividend yield to outpace the present inflation charge, a beautiful valuation, and the potential for future share worth progress.

In actual fact, it’s not solely Morgan Stanley who favors these names. Utilizing the TipRanks database, we discovered that each are additionally rated as ‘Sturdy Buys’ by the analyst consensus. Let’s take a better look.

Philip Morris Worldwide (PM)

We’ll begin with one of many best-known names within the ‘sin sector,’ Philip Morris Worldwide. This can be a chief within the tobacco trade, and the proprietor, with full manufacturing and advertising and marketing rights, of the Marlboro cigarette model’s worldwide footprint. A number of the firm’s different model names embody L&M, Chesterfield, and Subsequent, together with – you guessed it – Philip Morris. The corporate has a presence in over 175 world markets, and might boast that, in most of them, it holds the first- or second-place market share for cigarettes and different tobacco merchandise.

These main market shares are stable belongings, as a result of even with the rising social pressures towards smoking, the tobacco trade totaled some $867 billion in 2022 – and by the tip of this decade, the trade is predicted to hit a price of $1.05 trillion.

One of many chief results of anti-smoking strain, be they social or political, has been to push Philip Morris towards elevated diversification of its product strains. The corporate is a frontrunner not simply in cigarettes but additionally within the increasing marketplace for smokeless tobacco merchandise. Over the previous few years, PM has invested over $10.5 billion into such merchandise, and the corporate has seen smokeless non-nicotine merchandise improve their share of complete income from 29.1% in 2021 to almost 35% in 2022. The corporate is focusing on 50% of revenues from smoke-free merchandise by 2025. PM’s portfolio of smokeless merchandise contains the rising line of iQOS heated tobacco merchandise, a number of e-vape merchandise, and a variety of oral smokeless tobaccos.

Philip Morris will launch its monetary outcomes for 3Q23 later this month, however we are able to look again at Q2 and get an thought of simply the place the corporate stands. The second quarter top-line got here in at a hair below $9 billion, rising 14.5% year-over-year and beating the forecast by greater than $259 million. The agency’s backside line determine, a non-GAAP EPS of $1.60, was 12 cents per share higher than had been anticipated.

Wanting forward, the Avenue expects to see revenues of $9.31 billion and a non-GAAP EPS of $1.61 when PM releases its Q3 outcomes on October 19.

Rising revenues and earnings are supporting a stable dividend, which PM raised in its final declaration. The announcement, on Sept 13, set the widespread share quarterly dividend at $1.30 per share, for a 2.4% improve from the earlier payout. The annualized charge of $5.20 offers a yield of 5.6%, nicely above the final reported annualized inflation charge, of three.67% in August.

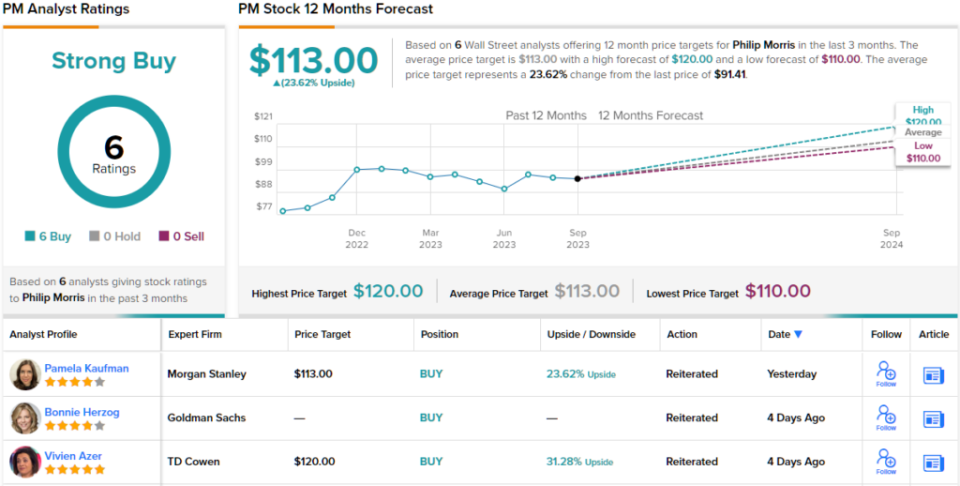

Protecting this inventory for Morgan Stanley, analyst Pamela Kaufman focuses on the corporate’s shift from cigarettes to smokeless tobacco as the important thing level for traders to think about going ahead. She writes, “PM is our High Choose as its peer-leading progress outlook is supported by its profitable transition to smoke-free merchandise and displays: 1) accelerating HTU (heated tobacco models) share from IQOS ILUMA rollout; 2) continued speedy Zyn progress within the US; 3) a big and engaging US progress alternative for IQOS with average funding wants; and 4) alternative for EBIT margin growth. We imagine valuation at 11x 2024 EV/EBITDA is engaging.”

Kaufman’s bullish stance helps her Obese (i.e. Purchase) ranking on the inventory, whereas her $113 worth goal signifies her confidence in ~24% one-year upside potential for the shares. Including within the dividend, and the overall return on this inventory is ~29% for the 12 months forward. (To observe Kaufman’s observe report, click here)

General, all 6 of the latest analyst critiques on this tobacco firm are optimistic, making for a unanimous Sturdy Purchase consensus ranking. PM shares are priced at $91.41, and their $113 common worth goal implies ~24% upside heading out to the one-year horizon. (See PM stock forecast)

Bridge Funding Group (BRDG)

Subsequent up, Bridge Funding Group, is an actual property funding belief, or REIT, a category of corporations lengthy often called ‘dividend champs.’ Bridge is a vertically built-in actual property supervisor, and its portfolio incorporates a variety of economic devices and properties. These embody real-estate-backed credit score, together with residential properties, places of work areas, logistics properties, and industrial-use web leased actual property.

Not solely is Bridge’s portfolio numerous in its broad classes, however the firm additionally works arduous to develop diversified holdings inside every class. The logistic properties, for instance, embody warehouses and transport hubs, and the corporate’s developments embody EV charging, LED lighting, and solar energy installations every time possible. Bridge’s residential properties embody single-family leases, senior housing, and multi-family residences. And within the credit score area, Bridge makes use of quite a lot of methods to assemble a various set of MBS belongings.

On the backside line, all of this added as much as distributable earnings of 20 cents per share within the firm’s 2Q23 monetary launch, based mostly on a web complete of $35 million. This was in-line with expectations. Dividend traders ought to be aware that Bridge has a historical past of adjusting its payout to maintain it in-line with distributable earnings. The present dividend, of 17 cents per share, annualizes to 68 cents per widespread share, and provides a yield of seven.4%, greater than sufficient to make sure an actual charge of return in right now’s setting.

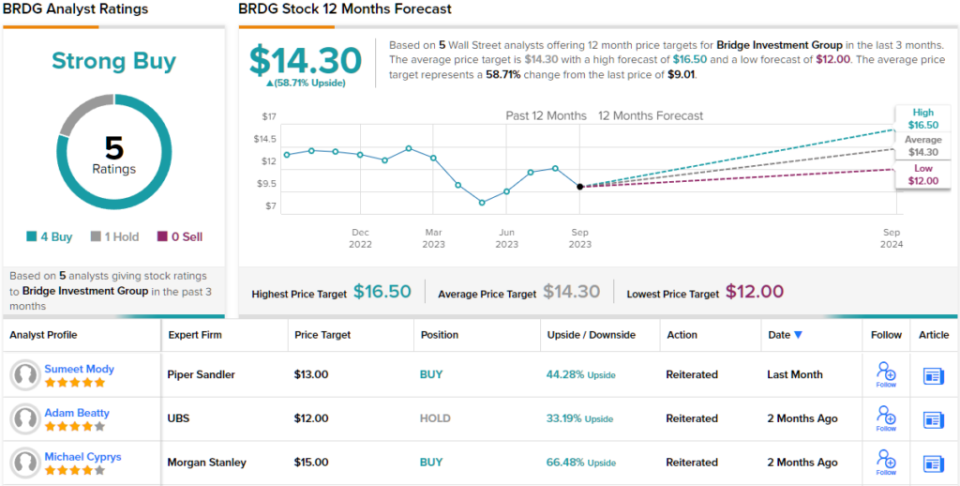

This firm’s dividend is engaging, however Morgan Stanley’s Michael Cyprys takes a better have a look at Bridge’s publicity to industrial actual property (CRE). This can be a critical concern, as CRE is flashing hazard indicators in a number of essential city areas, however Cyprys sees cause to imagine that Bridge can climate this storm and proceed to ship returns to traders. He writes, “Personal markets actual property supervisor buying and selling at depressed valuation because of blanket negativity that stems from rising CRE dangers round debt refi and valuations. We predict the market ought to be extra discerning given BRDG has restricted principal & redemption danger and as an alternative earns charges on locked-up, dedicated third get together capital. Whereas progress slows near-term (slower fundraising and transactional exercise), we nonetheless count on mid-teens progress in belongings and FRE. Fed pause might catalyze pickup in exercise later in ’23/into ’24, significantly if charges volatility is dampened.”

These feedback again up Cyprys’ Obese (i.e. Purchase) ranking on the inventory together with his $15 worth goal suggesting a achieve of ~66% within the 12 months forward. (To observe Cyprys’ observe report, click here)

General, this inventory will get a Sturdy Purchase consensus ranking, based mostly on 5 critiques that embody 4 to Purchase and 1 to Maintain. Shares are buying and selling for $9.01 with a mean goal worth of $14.30 to indicate ~59% one-year upside potential. (See BRDG stock forecast)

To search out good concepts for dividend shares buying and selling at engaging valuations, go to TipRanks’ Best Stocks to Buy, a newly launched instrument that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is vitally essential to do your individual evaluation earlier than making any funding.