Traders are continually searching for methods to generate stable returns, in spite of everything, that’s the entire level of investing. Reaching that purpose is less complicated mentioned than finished, nevertheless. As with something, if it had been actually easy, buyers would solely have success tales to inform.

That mentioned, there are methods to achieve an edge out there, and one widespread route is to maintain monitor of insiders’ actions. Insiders are the high-level firm officers, Board members, CFOs and COOs, as much as CEOs, whose positions give them a close-up data of their companies’ inside workings – and so they do commerce on that data.

Now, their trades can contain each shopping for and promoting, and what buyers want to recollect is that insiders solely have one cause to purchase their very own inventory – they suppose it should acquire worth. It’s as clear a sign as any investor may need.

And when the insiders begin spending thousands and thousands on their shares, that sign will get even clearer.

That’s what we’re seeing now, utilizing the Insiders’ Hot Stocks tool. Insiders have been pouring thousands and thousands into two dividend shares, signaling a powerful confidence of their long-term potential.

In reality, these insiders aren’t the one ones considering the time is true for loading up. A number of Wall Road analysts are additionally bullish on these equities, additional bolstering the case for funding. Let’s take a better look.

ExxonMobil (XOM)

The primary inventory we’ll have a look at is ExxonMobil, a pacesetter among the many world’s high ten largest oil firms. With a market cap of $433 billion, Exxon reported revenues within the neighborhood of $390 billion final 12 months.

The corporate is a serious operator within the discovery, manufacturing, and supply of hydrocarbon vitality assets, with a diversified portfolio that features numerous different important actions. ExxonMobil is a key provider of commercial chemical substances, and its gasoline merchandise are extensively used within the building and manufacturing sectors. Moreover, it’s contributing to the event of recent, light-weight plastics utilized in a mess of merchandise, from smartphones to airliners.

ExxonMobil operates in each the US and worldwide markets. Earlier this 12 months, it introduced a big growth in its oil manufacturing off the coast of Guyana. The corporate has obtained authorities approval for the Uaru, the fifth venture within the Stabroek block, an enhancement anticipated to generate a further quarter-million {dollars} in income per day, with a deliberate startup in 2026.

In July, Exxon introduced its acquisition of Denbury, an revolutionary firm within the carbon seize and oil restoration section. The Denbury acquisition will improve ExxonMobil’s capability for low carbon options, reflecting the oil firm’s dedication to a cleaner future.

Turning to the monetary aspect, we discover that Exxon posted $82.9 billion in complete income for 2Q23, reported on the finish of July. This complete was down by 28% from the year-ago quarter, and missed the forecast by $7.4 billion. The underside line earnings additionally got here in under expectations. The EPS determine of $1.94 per share was 8 cents decrease than had been anticipated. The misses had been influenced by headwinds within the hydrocarbon trade, together with falling costs within the first half of this 12 months.

Despite the fact that revenues and earnings had been down, ExxonMobil retained its means to generate sturdy money flows. The corporate had $9.4 billion in money movement from operations in Q2, and a free money movement of $5 billion.

Sound money flows assist to take care of the dividend, which Exxon will subsequent pay out to widespread shareholders on September 11. The cost is about at 91 cents per widespread share, and the annualized price of $3.64 provides an above-average yield of three.4%.

insider activity, we uncover a notable purchase made by Jeffrey Ubben, a member of the Board of Administrators, earlier this week. Ubben dropped a powerful $48.97 million to purchase 458,000 shares of XOM. Ubben stake within the firm totals over $175 million.

On the analyst entrance, Piper Sandler’s 5-star analyst Ryan Todd notes the disappointing headlines from the earnings report – but additionally notes that the corporate has strengths, together with its means to generate money and the probability of upper vitality costs in 2H23.

“Whereas each the headline earnings and upstream efficiency are disappointing, this was offset barely by money movement dynamics that had been stronger than anticipated. Much like friends, international gasoline headwinds had been important, nevertheless we anticipate many 2Q headwinds to reverse in 2H23, together with gasoline pricing, refining margins (already +15%-30% vs. 2Q), and chemical substances. And with structural value financial savings ($8.3B to this point) driving practically 2x the profitability, we anticipate XOM to proceed to drive relative outperformance,” Todd opined.

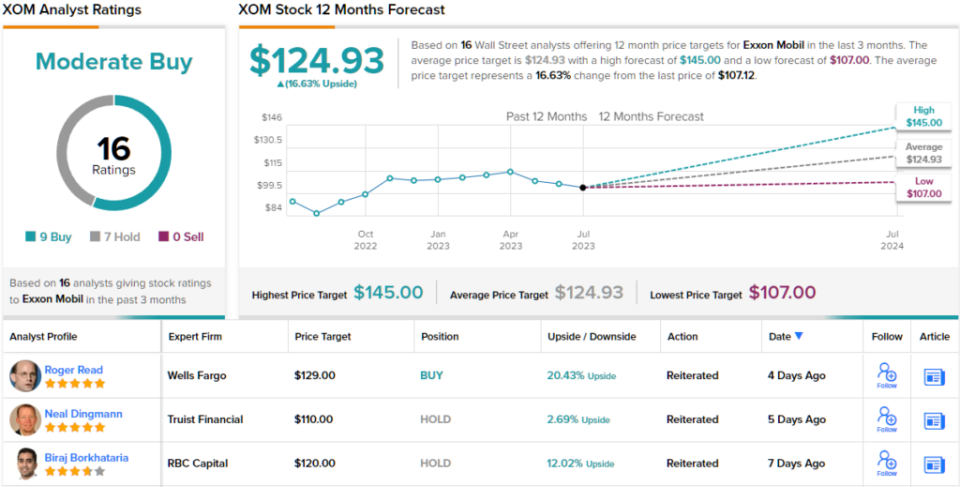

These feedback again up Todd’s Chubby (i.e. Purchase) ranking on XOM, and his $127 value goal signifies his perception in an 18.5% upside potential for the shares. Based mostly on the present dividend yield and the anticipated value appreciation, the inventory has ~22% potential complete return profile. (To look at Todd’s monitor document, click here)

General, this oil main will get a Reasonable Purchase ranking from the Road’s consensus, based mostly on 16 current analyst critiques that embrace 9 Buys and seven Holds. The shares are priced at $107.12, with a median value goal of $124.93 to recommend ~17% one-year upside potential. (See XOM stock forecast)

Agree Realty Company (ADC)

From oil majors, we’ll shift focus to the true property funding belief (REIT) section, the place Agree Realty, based mostly within the Metro Detroit space, operates via the acquisition, possession, and administration of a variety of actual properties.

Agree’s portfolio is each worthwhile and extremely diversified. As of the top of 2Q23, Agree had 2,004 properties in its portfolio, positioned in 49 states, and totaling 41.7 million sq. ft of leasable space. The corporate’s portfolio was 99.7% leased on the finish of Q2, with the investment-grade retail tenants producing 67.9% of the annualized base rents.

Along with conventional actual properties, Agree additionally invests in floor leases, and in Q2, the corporate acquired three extra of those properties for a complete buy value of $25.8 million. These introduced the corporate’s floor lease portfolio as much as 210 leases, with a complete of 5.7 million sq. ft of gross leasable space. The bottom lease portfolio was absolutely occupied on the finish of Q2 and had a weighted common remaining lease time period of practically 11 years.

This all interprets to a portfolio able to producing stable income – Agree posted a high line of $129 million for Q2, up 24% year-over-year and modestly $58K higher than the estimates. The corporate’s internet revenue per share, at 42 cents, was down over 7% y/y, and was a penny decrease than anticipated.

Certainly one of Agree Realty’s standout options is its fame for offering a dependable month-to-month dividend payout. The most recent declared dividend stands at $0.243 per widespread share, leading to an annualized cost of $2.916 and a horny yield of 4.5%.

Current insider exercise additional reinforces a optimistic outlook on the corporate. Three insiders, together with the CEO and government chairman of the board, made ‘informative purchase’ transactions earlier this week, investing a complete of over $3.25 million within the firm’s inventory. Particularly, Board member John Rakolta spent $1.89 million on 30,000 shares of ADC inventory, CEO Joey Agree spent $627,900 to purchase 10,000 shares, and at last, government chairman – and firm founder – Richard Agree picked up 11,751 shares for $739,725.

Truist analyst Ki Bin Kim additionally shares a good view of Agree Realty. Kim is impressed by the corporate’s share worth, and its stability sheet – and by administration’s confirmed competence. He says of this inventory, “We stay BUY rated resulting from: 1) enticing valuation, 16.5x 2023 P/AFFO; 2) inventory has already considerably underperformed triple internet friends this 12 months -8.9% vs. -2.4%; 3) draw back safety by way of 68% IG tenancy; 4) sturdy stability sheet and mgmt. monitor document.”

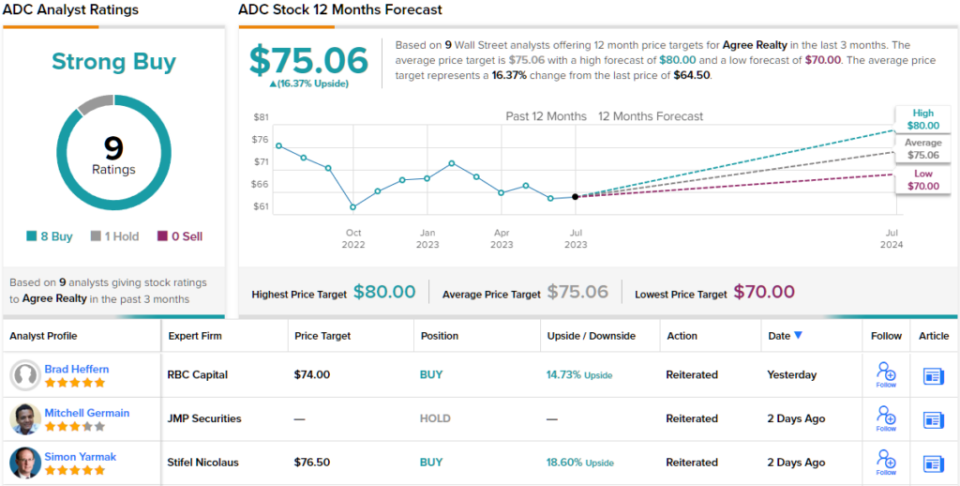

Wanting forward, Kim charges ADC a Purchase, and his $77 value goal means that he sees a 20% upside on the one-year horizon. (To look at Kim’s monitor document, click here)

General, the 9 current analyst critiques right here break down 8 to 1 in favor of Buys over Holds, giving ADC its Sturdy Purchase consensus ranking. The shares are at present buying and selling for $64.50 and their $75.06 common value goal implies a 16% upside for the following 12 months. (See ADC stock forecast)

To search out good concepts for shares buying and selling at enticing valuations, go to TipRanks’ Best Stocks to Buy, a software that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is vitally essential to do your personal evaluation earlier than making any funding.