Many traders have an interest within the “Magnificent Seven” stocks for good causes apart from excellent returns during the last 12 months. This elite group of tech corporations has robust manufacturers and a rising buyer base, and they’re very worthwhile companies — all the pieces an investor appears to be like for in a stable funding.

During the last 12 months, the Roundhill Magnificent Seven ETF has returned 51%, beating the Nasdaq Composite‘s 32% and the S&P 500‘s 23% return. There’s some debate about how lengthy this group will proceed to outperform within the close to time period. On a price-to-earnings (P/E) foundation, most of those shares commerce at massive premiums to the common inventory within the main indexes.

The costliest of the seven is Nvidia (NASDAQ: NVDA), which at present has a trailing P/E of 77. Regardless of its excessive valuation, the corporate’s superior progress and future alternative may justify extra new highs for years to come back. This is why the inventory stays a core holding in my portfolio.

Nvidia’s progress runway

Nvidia is benefiting as information facilities change from central processing items (CPUs) to the much more highly effective graphics processing units (GPUs) for synthetic intelligence (AI) workloads. Traditionally, information facilities spent about $250 billion per 12 months on infrastructure, however this quantity has elevated for the primary time in a few years, which might be only the start of a serious spending growth.

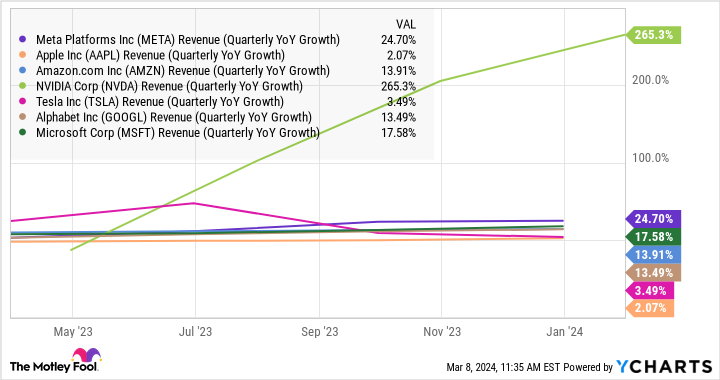

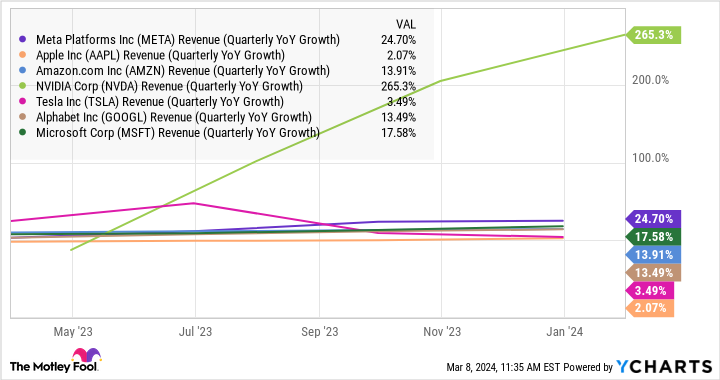

The marketplace for Nvidia’s merchandise is proving to be a lot greater than initially thought a number of years in the past. Income surged 265% 12 months over 12 months to $22 billion within the fiscal fourth quarter, considerably outpacing the expansion for the opposite Magnificent Seven corporations.

Nvidia is simply scratching the floor of this chance. Firm executives have talked about $1 trillion value of knowledge heart infrastructure that’s beginning to undertake accelerated computing, which is the usage of a number of GPUs operating collectively to deal with giant information workloads.

Nevertheless, the chance might be a lot greater. AI is permitting corporations to make use of information in ways in which was not attainable earlier than, as Nvidia chief monetary officer Colette Kress mentioned on the latest Morgan Stanley know-how convention.

Because of this there are new kinds of information facilities rising known as GPU-specialized cloud service suppliers. It is one purpose Nvidia executives consider the precise information heart infrastructure market might be value nearer to $2 trillion.

Why purchase the inventory?

AI is totally turning conventional computing on its head, which is mirrored within the accelerating demand for Nvidia’s H100 GPU. It is virtually develop into a bragging proper for corporations to speak about what number of H100s they’ve bought. Magnificent Seven member Meta Platforms has mentioned it plans to have 350,000 H100s up and operating by the tip of the 12 months.

Demand is already outstripping provide for Nvidia’s H200 GPU, which is on observe to begin delivery within the fiscal second quarter. Firm steering requires income to be up 234% 12 months over 12 months within the fiscal first quarter.

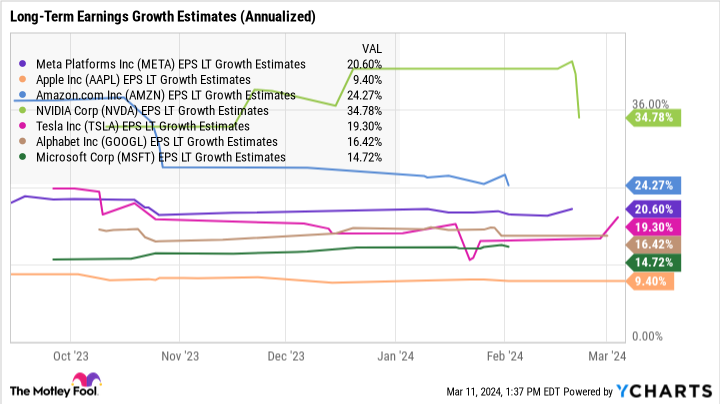

Over the long run, analysts count on Nvidia to develop earnings at 35% per 12 months, which can also be greater than the opposite Magnificent Seven.

Nvidia’s main share within the GPU market ought to translate to extra progress as information facilities proceed to improve parts for AI. As this chance unfolds, this GPU inventory gives long-term upside that might outperform the opposite Magnificent Seven over the following decade. Relative to anticipated earnings this 12 months, Nvidia is not all that costly, buying and selling at a ahead P/E of 37.

Nvidia has been the king of GPUs for a few years, so it is principally obtained the suitable product on the proper time to learn from the AI growth. However what finally seals the deal for me is how a lot money the enterprise is producing.

Its trailing free money circulate totaled $27 billion, up 10-fold during the last 5 years. This provides the corporate great assets to remain forward in GPU innovation and generate shareholder returns for years to come back.

Do you have to make investments $1,000 in Nvidia proper now?

Before you purchase inventory in Nvidia, think about this:

The Motley Idiot Inventory Advisor analyst crew simply recognized what they consider are the 10 best stocks for traders to purchase now… and Nvidia wasn’t one in every of them. The ten shares that made the minimize may produce monster returns within the coming years.

Inventory Advisor gives traders with an easy-to-follow blueprint for fulfillment, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than tripled the return of S&P 500 since 2002*.

*Inventory Advisor returns as of March 11, 2024

John Mackey, former CEO of Complete Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. Randi Zuckerberg, a former director of market growth and spokeswoman for Fb and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Idiot’s board of administrators. Suzanne Frey, an govt at Alphabet, is a member of The Motley Idiot’s board of administrators. John Ballard has positions in Nvidia and Tesla. The Motley Idiot has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Idiot recommends the next choices: lengthy January 2026 $395 calls on Microsoft and quick January 2026 $405 calls on Microsoft. The Motley Idiot has a disclosure policy.

Here’s My Top “Magnificent Seven” Stock to Buy and Hold for the Next 10 Years was initially printed by The Motley Idiot