We are now in the busiest week of this earnings season, and among others, five Magnificent 7 stocks will report their quarterly earnings. Fintech giant SoFi (SOFI) will release its Q1 earnings on April 29, before the markets open. While the S&P 500 Index ($SPX) has soared to record highs, defying pessimism over higher energy prices and the fragile Middle East truce, SoFi is down over 43% from its all-time high and has lost nearly 30% this year alone. Let’s look at SoFi’s Q1 2026 earnings estimates and analyze whether the stock is a buy before the report.

SoFi Q1 2026 Earnings Estimates

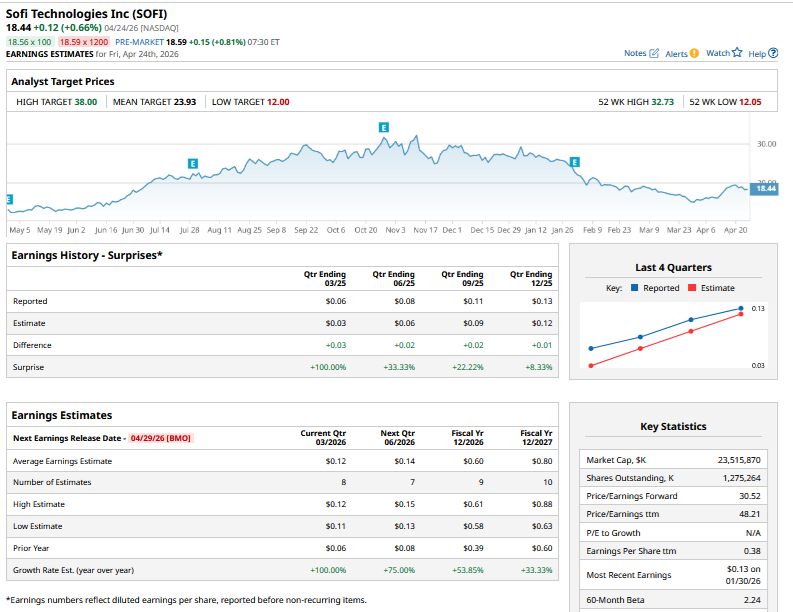

Analysts expect SoFi to post revenues of $1.05 billion in Q1, a year-over-year (YoY) rise of 36.1%, and in line with the company’s guidance. Consensus estimates call for SoFi’s adjusted earnings per share (EPS) to double to 12 cents, which is also in line with the company’s guidance. Given that SoFi has historically been quite conservative with its guidance, I won’t be surprised if the company ends up beating Q1 estimates. That said, a beat won’t necessarily mean a rally, as SOFI stock plunged following the Q4 2025 report despite beating on both the topline and the bottomline, with weakness in the Tech Platform business and ongoing concerns over a previously announced capital raise spooking investors.

More News from Barchart

What to Watch in SoFi’s Q1 Earnings?

Apart from the headline numbers, I will watch out for the following in SoFi’s Q1 earnings call.

-

Update on Muddy Water report: In March, short seller Muddy Water accused SoFi of accounting malpractices. SoFi, however, dismissed these claims and said that they “demonstrate a fundamental lack of understanding of our financial statements and business.” It also talked about exploring legal action against Muddy Waters, but we haven’t heard from the company since. During the Q1 earnings call, SoFi might provide an update on any legal recourse it is seeking. Furthermore, I believe it might be an opportunity for SoFi to brief markets about its accounting practices, as some of these, particularly on the fair value of assets, have been a concern for a section of the market.

-

Delinquencies: Given the deterioration in the macro environment, I will watch out for the delinquency numbers in SoFi’s Q1 earnings call. It would also be prudent to hear the management’s commentary on the health of the consumer, as the company has a significant exposure to unsecured personal loans.

-

Guidance: During the Q4 2025 earnings call, SoFi guided for a 30% YoY rise in 2026 revenue and members. It expects to generate an adjusted earnings before interest, tax, depreciation, and amortization (EBITDA) of $1.6 billion, which represents a healthy margin of 34%. Management forecasts full-year adjusted EPS at $0.60, which is 53% higher than the $0.39 it posted last year. During the earnings call, I will watch out for any revision to that guidance, given the current macro environment.