(Bloomberg) — The heart beat of US inflation possible continued to gradual at first of the 12 months, serving to to feed expectations that the Federal Reserve will discover interest-rate cuts extra palatable within the coming months.

Most Learn from Bloomberg

The core shopper value index, a measure that excludes meals and gas for a greater image of underlying inflation, is seen rising 3.7% in January from a 12 months earlier.

That will mark the smallest year-over-year advance since April 2021, and underscore the inroads Fed Chair Jerome Powell and his colleagues have made in beating again inflation. The general CPI in all probability rose lower than 3% for the primary time in almost two years, economists forecast Tuesday’s report to point out.

Whereas acknowledging that progress, policymakers have been cool to the concept charges could also be decreased as quickly as subsequent month.

Learn Extra: Fed Officers Add to Refrain Tempering Hopes for Price Cuts Quickly

Their endurance has roots in an financial system that’s flashing inexperienced lights, the most important of which is the labor market. Sturdy employment progress has stored customers spending. A separate report on Thursday is projected to disclose one other enhance in retail gross sales, excluding motor autos and gasoline.

The cooling of inflation, together with expectations that borrowing prices will head decrease this 12 months, explains the latest enchancment in shopper confidence. A College of Michigan survey scheduled for launch on Friday is forecast to point out an index of sentiment holding close to the best stage since July 2021.

Buyers can even monitor Fed officers talking within the days following the CPI information, to gauge the timing of any future fee lower. Amongst these on the schedule are regional financial institution presidents Raphael Bostic of Atlanta and Mary Daly of San Francisco, who each vote on coverage this 12 months.

What Bloomberg Economics Says:

“In deciding when to begin chopping charges, the Fed must reconcile the info they’ve in hand – which present inflation on a quick monitor to the two% goal — with dangers that inflation might flare up once more or the labor market might weaken extra sharply. Information within the coming week will issue into that call — however received’t present a definitive reply.”

— Anna Wong, Stuart Paul, Eliza Winger and Estelle Ou, economists. For full evaluation, click on right here

Turning north, Canadian residence gross sales will reveal whether or not the market continues to warmth up forward of anticipated mid-year fee cuts. Housing begins and manufacturing information can even be launched.

Amongst world highlights this week, Japanese gross home product, UK inflation and wages, and testimony by the euro-zone central financial institution chief will function.

Click on right here for what occurred final week and beneath is our wrap of what’s developing within the world financial system.

Asia

Japan’s financial system is anticipated to rebound from its dismal efficiency over the summer time, offering one other sign for the Financial institution of Japan because it prepares to finish its destructive fee coverage.

Figures out Thursday are additionally set to substantiate that Japan has slipped to the fourth-largest financial system on the planet, behind the US, China and Germany.

China’s markets can be closed for Lunar New 12 months celebrations, and no main releases are scheduled.

Reserve Financial institution of India Governor Shaktikanta Das, who stored a hawkish stance at Thursday’s fee assembly, may even see some progress in his inflation struggle at first of the week with shopper costs anticipated to have grown at a slower tempo in January. That in all probability received’t be gradual sufficient to immediate speak of a pivot, nevertheless.

The Philippine central financial institution is seen holding charges regular on Thursday after costs continued to weaken there too.

Australian jobs figures earlier within the day are seen exhibiting a return to progress after the losses in December.

Singapore will revise its gross home product figures forward of commerce information the next day.

RBNZ Governor Adrian Orr units out his newest place on coverage and a pair of% inflation in a speech Friday morning, with Malaysian GDP numbers closing out the week.

Europe, Center East, Africa

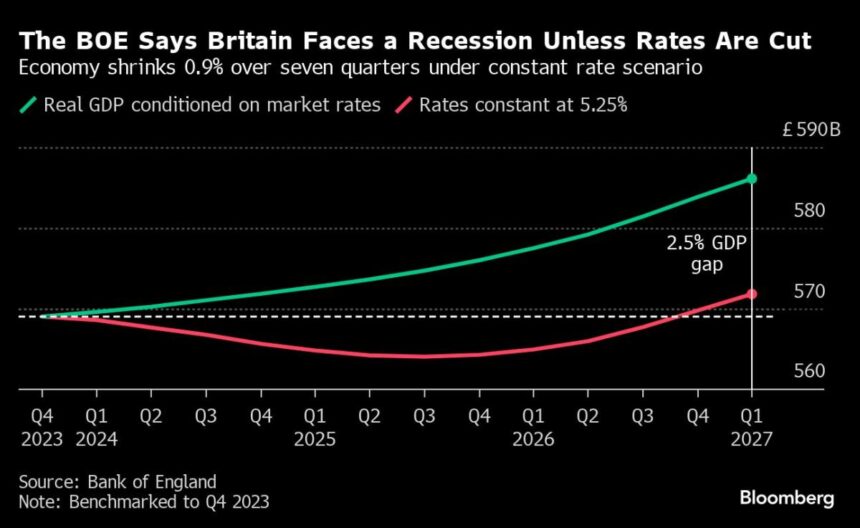

UK information will take the limelight. On Tuesday, wage numbers might present the weakest pay pressures since 2022, cheering Financial institution of England officers who — like world friends — are pivoting towards fee cuts.

Policymakers can even scrutinize an anticipated blip increased in inflation on the headline gauge, and the core measure that strips out risky parts corresponding to vitality, in information due Wednesday.

The following day, GDP will level to how BOE tightening is hitting progress. Economists reckon the UK stagnated within the fourth quarter, narrowly avoiding a recession for now.

Inflation information for January can even be launched across the wider area this week:

-

Swiss consumer-price progress in all probability slowed to 1.6%, whereas Denmark will launch equal numbers.

-

In Japanese Europe, inflation is anticipated to have weakened markedly in Poland and the Czech Republic, whereas edging increased in Romania.

-

In Ghana, the speed is more likely to have eased from 23.2% a month earlier, whereas Nigeria’s studying might have accelerated from 28.9% amid foreign money weak point.

-

And in Israel, inflation is anticipated to have slowed to 2.7%.

A sequence of fourth-quarter GDP numbers are additionally scheduled, with progress in Japanese European economies and Norway as nicely more likely to have stayed subdued.

Euro-zone industrial manufacturing on Thursday is a spotlight within the foreign money area, with a fourth month-to-month drop in December predicted by economists amid falling manufacturing facility output in economies together with Germany.

Policymaker appearances will draw consideration. European Central Financial institution President Christine Lagarde testifies to lawmakers on Thursday, whereas a number of occasions that includes her colleagues are additionally scheduled.

Talking this weekend, ECB Governing Council member Fabio Panetta stated “the time for reversal of the financial coverage stance is quick approaching,” warning in opposition to ready too lengthy on fee cuts.

In Norway, Governor Ida Wolden Bache will make her annual tackle to Norges Financial institution’s supervisory council.

A handful of fee selections are on the calendar all through the broader area:

-

In Romania on Tuesday, the central financial institution will in all probability hold its fee at 7% as buyers look ahead to clues on potential cuts.

-

Zambian officers are poised to boost borrowing prices on Wednesday to assist a battered foreign money and curb mounting value pressures.

-

The identical day, Namibia’s policymakers will possible go away borrowing prices unchanged according to South Africa’s pause final month.

-

And on Friday, the Financial institution of Russia might keep on maintain after Governor Elvira Nabiullina indicated in December that the important thing fee will stay elevated for an prolonged interval to sort out inflation operating at virtually double the 4% goal.

Latin America

The Carnival vacation makes for a quiet begin to the week, however Argentina returns on Wednesday to submit its January inflation report.

Client costs possible rose 21.9% final month, based on economists surveyed by the central financial institution, down from 25% in December. That forecast implies an annual fee of over 250%, up from 211% at year-end 2023.

Inflation has surged within the wake of President Javier Milei’s 54% peso devaluation and elimination of value controls on a whole lot of on a regular basis shopper merchandise.

Colombia publishes a raft of knowledge, underscoring the precipitous slowdown in what had been one in every of Latin America’s post-pandemic vibrant lights.

Industrial output, manufacturing and retail gross sales have all been destructive since March, whereas fourth-quarter output in all probability shrank from the earlier three months. Full-year GDP progress might solely simply high 1%, nicely off the 2021 and 2022 readings of 11% and seven.5%.

Brazil posts December GDP-proxy figures forward of the quarterly and full-year report due March 1, whereas Peru publishes December financial exercise information together with January unemployment for Lima, the capital and largest metropolis.

Lastly, Chile’s central financial institution serves up the minutes of its January resolution to ship a 100 basis-point lower, to 7.25%. Economists surveyed by the central financial institution see that hitting 4.75% by year-end with inflation again at 3%.

–With help from Piotr Skolimowski, Robert Jameson, Monique Vanek, Brian Fowler, Abeer Abu Omar, Tony Halpin and Laura Dhillon Kane.

(Updates with Panetta in EMEA part)

Most Learn from Bloomberg Businessweek

©2024 Bloomberg L.P.