Observe: A model of this text was printed on TKer.co.

Shares rallied final week, with the S&P 500 climbing 1.3% to shut at 4,415.24. The index is now up 15% yr thus far, up 23.4% from its October 12, 2022 closing low of three,577.03, and down 7.9% from its January 3, 2022 file closing excessive of 4,796.56.

Whereas the overall data point out continued economic growth, there are indicators of stress growing that bear watching.

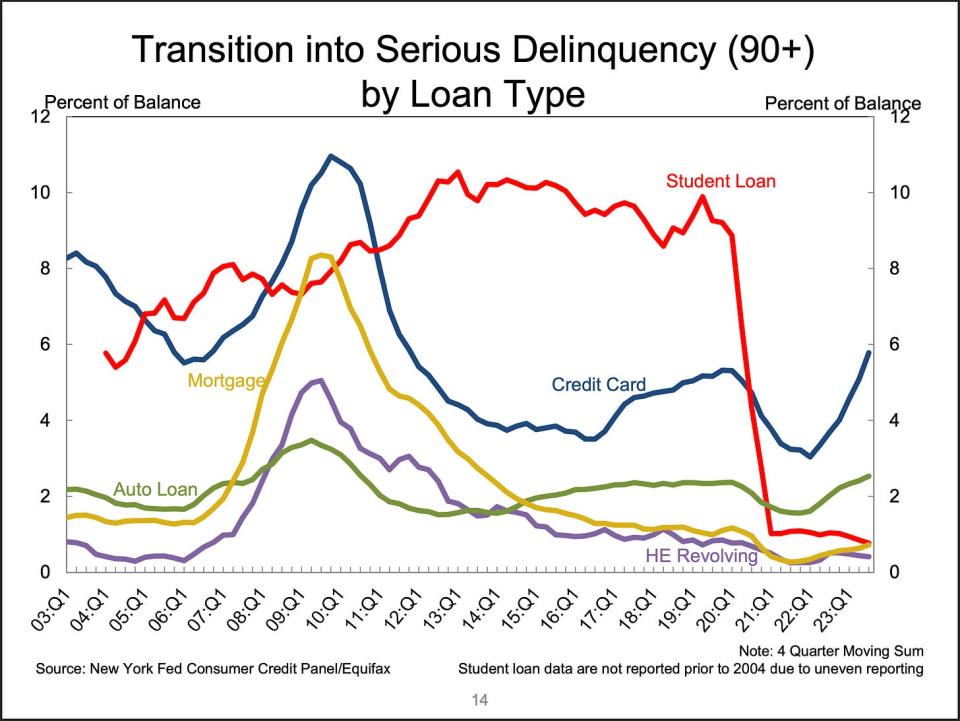

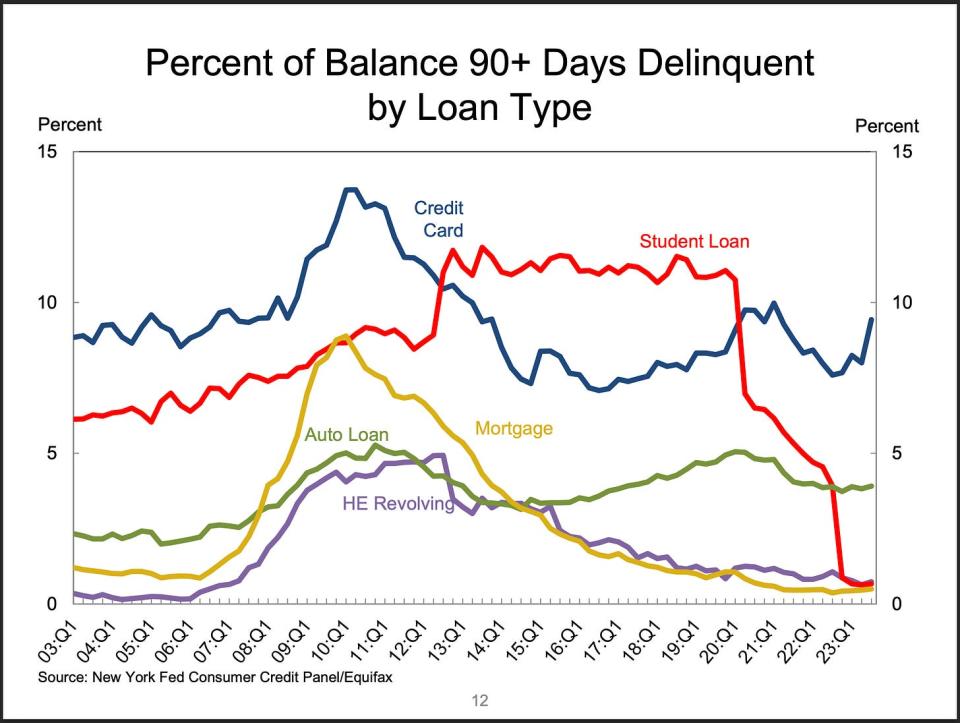

In response to the New York Fed’s Q3 Household Debt and Credit (HHDC) report, the share of debt newly transitioning into delinquency continues to rise for mortgages, auto loans, and bank cards.

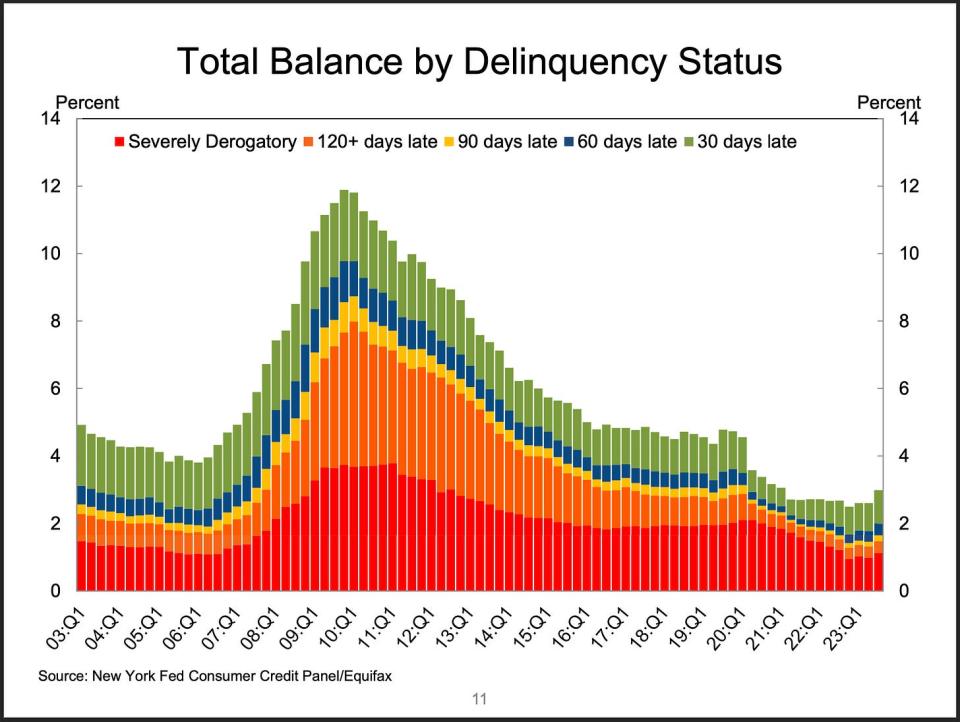

Once you embody the debt, the delinquency charges, whereas rising, proceed to replicate a normalization again to prepandemic ranges.

In different phrases, whereas the “circulation” into new delinquency has been choosing up, the “inventory” of delinquencies stays under prepandemic ranges.

“As of September, 3.0% of excellent debt was in some stage of delinquency, up by 0.4 share factors from the second quarter but 1.7 share factors decrease than the fourth quarter of 2019,” New York Fed researchers wrote.

The rise in delinquencies comes as banks have been tightening lending requirements.

In response to the Federal Reserve’s October Senior Loan Officer Opinion Survey on Financial institution Lending Practices, lending requirements have tightened for residential actual property loans…

… and for shopper loans.

In keeping with softening, however not notably unhealthy

There’s not a lot to rejoice right here, particularly if you’re a shopper that’s affected or you’re somebody hoping for warmer financial progress.

These deteriorating metrics, nevertheless, do seem in step with the Federal Reserve’s ongoing efforts to convey down inflation by reining the economy by tightening monetary policy. Certainly, key labor market metrics have been cooling for over a yr. Learn extra on the evolving labor market here, here, here, and here.

That mentioned, it’s additionally arguably untimely to conclude that the decelerating financial system is destined to transition into one which’s in an outright recession.

“Total this seems to be per a softening trajectory for shopper spending, however not a very unhealthy one,” JPMorgan’s Daniel Silver wrote in response to the HHDC report.

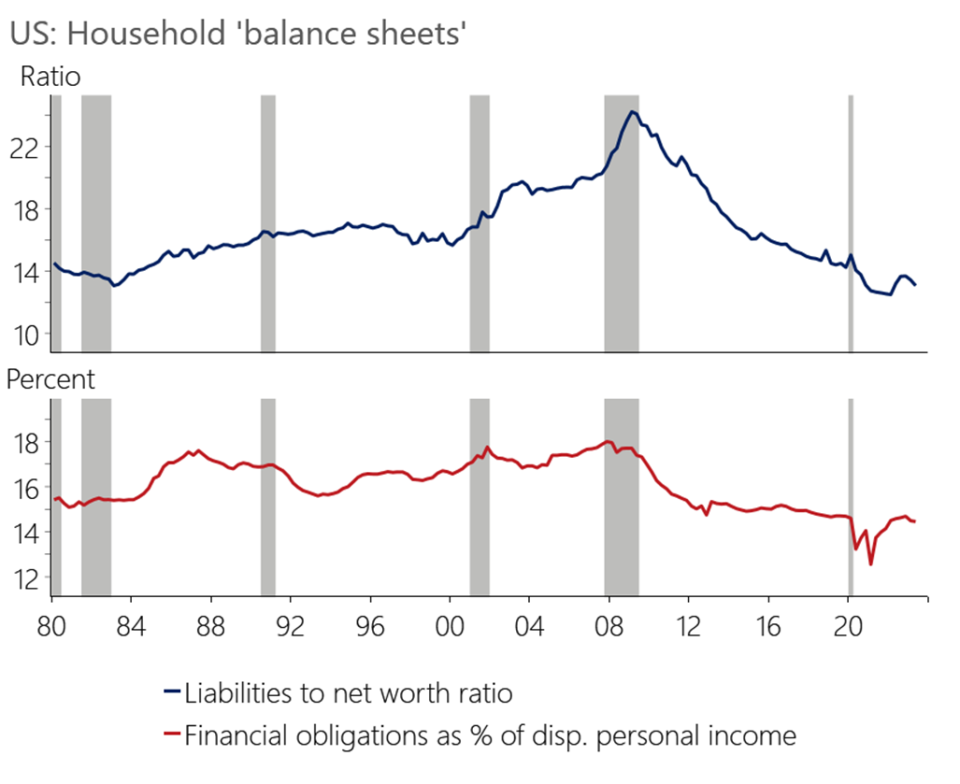

Make no mistake: Shopper funds proceed to be in remarkably good shape.

“We have now emphasised that family steadiness sheets look very sturdy after a protracted streak of deleveraging following the World Monetary Disaster, and this might cut back the necessity for many households to tighten their belts,” Oxford Economics’ Daniel von Ahlen wrote on Friday. “The surge in fairness and home prices because the pandemic imply that family web value is at file highs.”

Take into account that the deteriorating credit score metrics mentioned above occurred throughout a period of robust GDP growth, supported by resilient consumer spending growth. And the financial system continues to be supported by many other tailwinds pointing to extra progress forward.

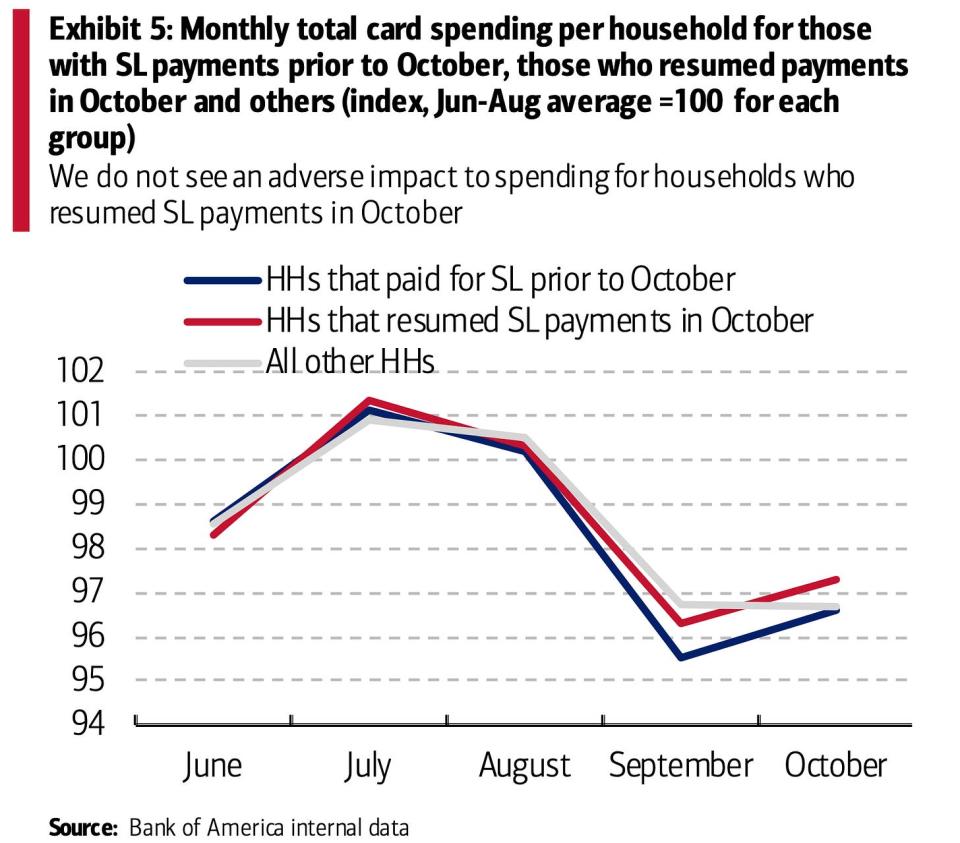

The restart of pupil mortgage funds have had restricted affect

Up to now, the resumption of student loan payments has had a restricted impact on the buyer image.

“We must also take into account that the 3Q [HHDC] report might be too early to see potential damaging results of the tip of forbearance on pupil loans, though the early learn from some associated information is that this seemingly won’t find yourself being an enormous drag on shoppers,” JPM’s Silver mentioned.

In response to JPMorgan’s evaluation, Chase Consumer Card spending information as of November 1 suggests the U.S. Census’ management measure of retail gross sales — which is utilized in calculating GDP progress — was up 0.52% month-over-month in October.

Citing their very own proprietary information, Bank of America analysts found card spending declined by 0.2% in October.

“With the tip of the scholar mortgage moratorium, many are questioning if shoppers will in the reduction of on spending to make mortgage repayments,” Financial institution of American analysts wrote. “Once we have a look at the spending of households who made a [student loan] cost for the primary time in 2023 in October, we don’t see any apparent signal of an antagonistic affect relative to different teams of households.”

For extra, learn: What the restart of student loan payments could mean for the economy 🎓

Be vigilant 👀

Simply because the stock market usually goes up and the economy is usually growing doesn’t imply they’re all the time doing so.

Bear markets and recessions are unfortunate hurdles on the long-run path to constructing wealth in danger belongings.

To reiterate, the overall data point out continued economic growth — and consequently recommend a bullish “Goldilocks” soft landing scenario the place inflation cools to manageable ranges without the economy having to sink into recession.

However as the info continues to return in, we’ll have to be vigilant as we look ahead to indicators that the economic narratives could also be shifting.

Reviewing the macro crosscurrents

There have been just a few notable information factors and macroeconomic developments from final week to contemplate:

Moody’s turns damaging on U.S. credit standing. On Friday, bond score company Moody’s modified its outlook for the U.S. authorities’s Aaa credit standing to “damaging from steady.” From Moody’s: “The important thing driver of the outlook change to damaging is Moody’s evaluation that the draw back dangers to the US’ fiscal energy have elevated and will not be totally offset by the sovereign’s distinctive credit score strengths. Within the context of upper rates of interest, with out efficient fiscal coverage measures to cut back authorities spending or enhance revenues, Moody’s expects that the US’ fiscal deficits will stay very giant, considerably weakening debt affordability. Continued political polarization inside US Congress raises the chance that successive governments will be unable to achieve consensus on a fiscal plan to sluggish the decline in debt affordability.”

A bond score company’s modified view on the U.S. often isn’t as huge a deal as it would sound.

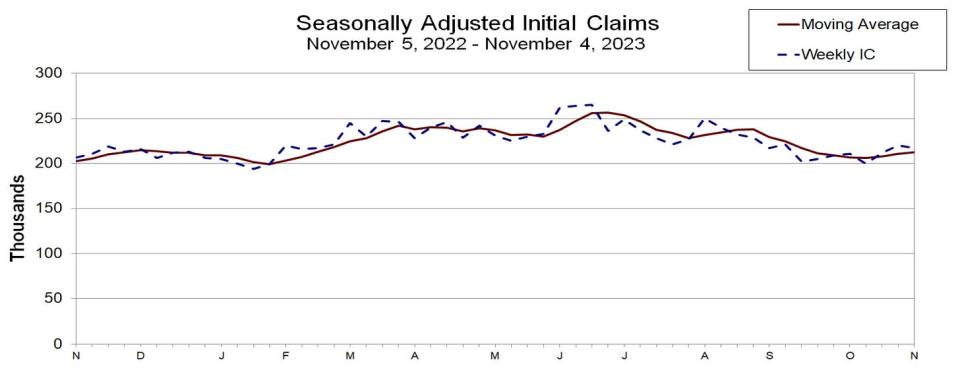

Unemployment claims tick down. Initial claims for unemployment benefits fell to 217,000 in the course of the week ending November 4, down from 220,000 the week prior. Whereas that is up from a September 2022 low of 182,000, it continues to development at ranges related to financial progress.

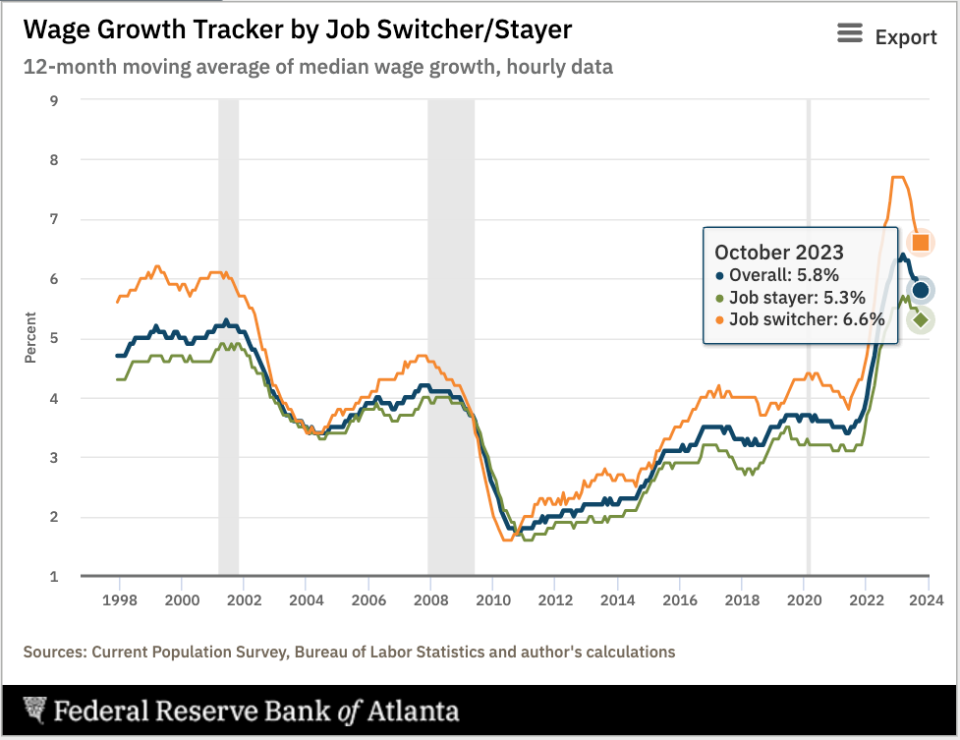

Job switchers lose pay benefit as wage progress cools. In response to the Atlanta Fed’s wage growth tracker, the hole wage progress between those that change jobs and people who keep at their jobs continues to shut. Job switchers noticed 6.6% wage progress within the 12 months ending in October, whereas job stayers noticed 5.3% progress in the course of the interval.

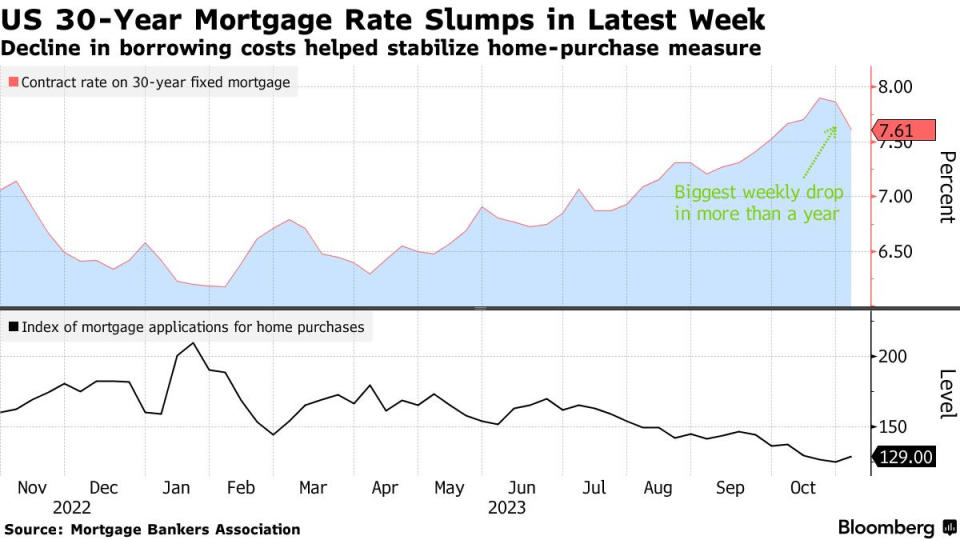

Mortgage charges fall, mortgage purposes rise. From Bloomberg: “The common 30-year mortgage price plunged final week by probably the most in additional than a yr, serving to generate the most important advance in house buy purposes since early June. The contract price on a 30-year mounted mortgage slid 25 foundation factors to 7.61%, the bottom stage because the finish of September, in accordance with the Mortgage Bankers Affiliation. The group’s index of mortgage purposes for house purchases elevated 3% within the week ended Nov. 3, the info out Wednesday confirmed.”

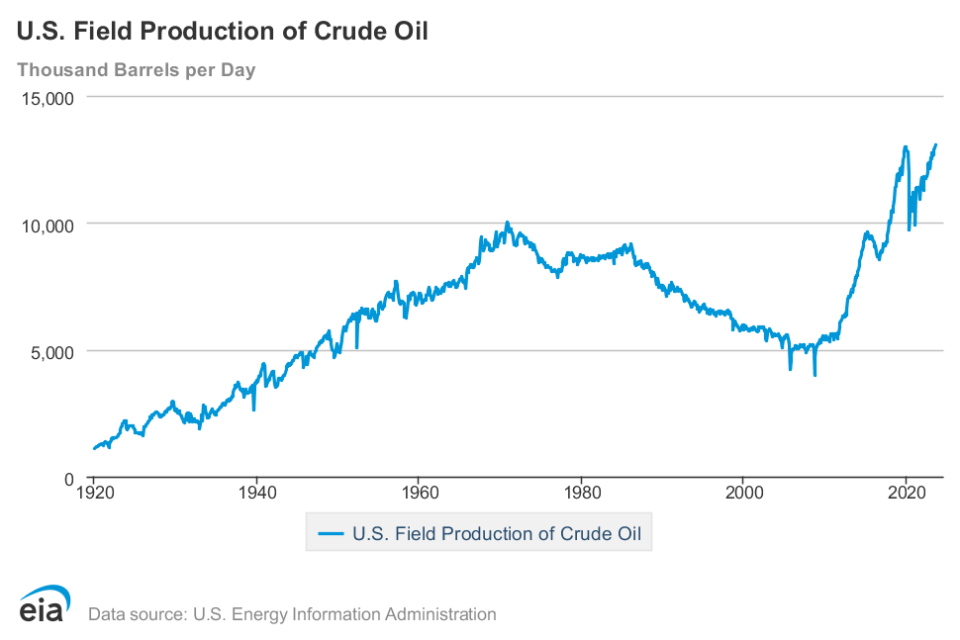

Pumping oil at a file tempo. From Bloomberg: “U.S. crude manufacturing jumped to a file excessive of 13.05 million barrels a day in August, the US Vitality Info Administration mentioned [Oct. 31] in a month-to-month report. The output surpassed a earlier excessive set in November 2019 of 13 million barrels a day. US crude has been enjoying an more and more important position in international oil markets due OPEC+ leaders Saudi Arabia and Russia extending manufacturing cuts.”

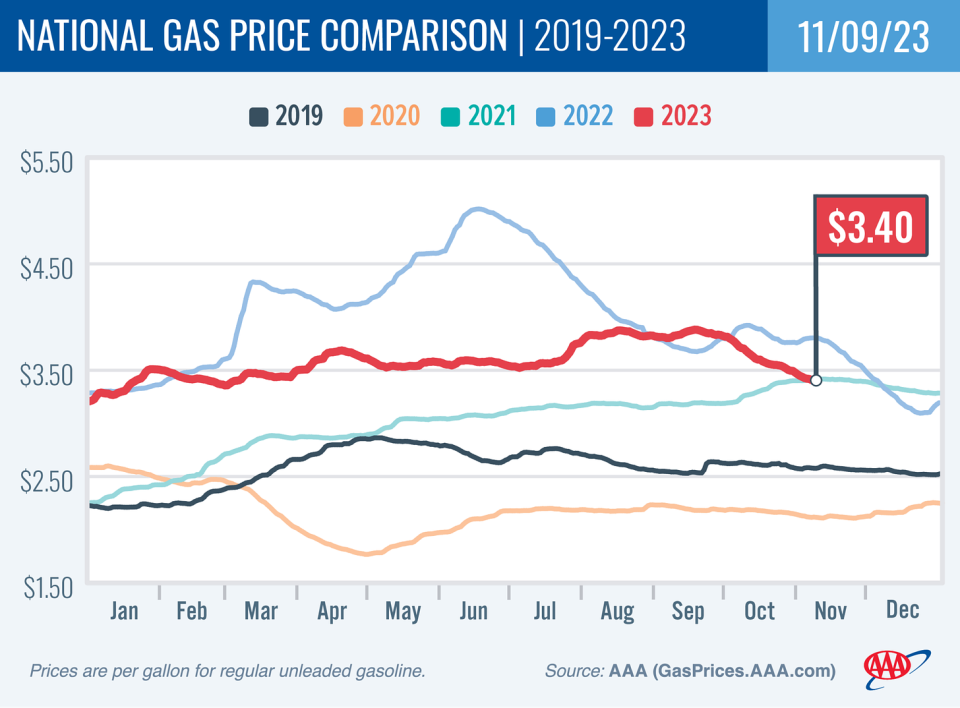

Gasoline costs fall. From AAA: “The nationwide common for a gallon of fuel dropped 4 cents since final week to $3.40. Nevertheless, the regular, if sluggish, decline might acquire pace after current drops within the worth of oil. Parked within the mid-$80s per barrel every week in the past, oil is now hovering across the mid-$70s. Since it’s the important ingredient in gasoline, cheaper oil often results in falling fuel costs.”

Right here’s an fascinating mind-set about fuel costs from Justin Wolfers: The variety of minutes of labor it takes to pay for a gallon of fuel.

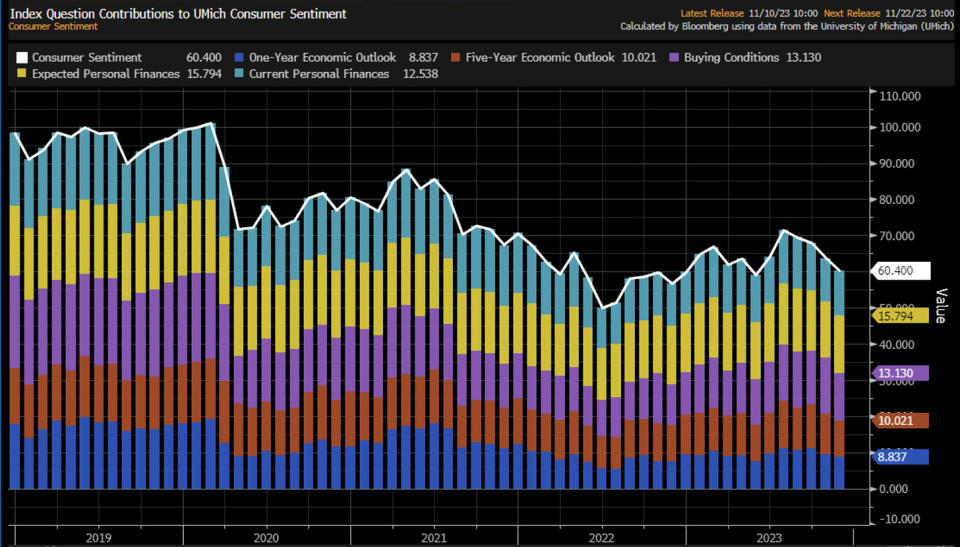

Shopper sentiment sours. From the College of Michigan’s November Surveys of Consumers: “Shopper sentiment slipped for the fourth straight month, falling 5% in November. Whereas present and anticipated private funds each improved modestly this month, the long-run financial outlook slid 12%, partly resulting from rising considerations concerning the damaging results of excessive rates of interest. Ongoing wars in Gaza and Ukraine weighed on many shoppers as nicely. Total, lower-income shoppers and youthful shoppers exhibited the strongest declines in sentiment. In distinction, sentiment of the highest tercile of inventory holders improved 10%, reflecting the current strengthening in fairness markets.”

Stock ranges are down. Wholesale inventories stood at $901.8 billion in September. The inventories/gross sales ratio was 1.33, down from 1.36 the earlier yr.

⛓️ Provide chain pressures loosen. The New York Fed’s Global Supply Chain Pressure Index — a composite of various provide chain indicators — ticked decrease in October and stays under ranges seen even earlier than the pandemic. That is means down from its December 2021 provide chain disaster excessive.

Close to-term GDP progress estimates stay constructive. The Atlanta Fed’s GDPNow model sees actual GDP progress climbing at a 2.1% price in This autumn.

Placing all of it collectively

We proceed to get proof that we might see a bullish “Goldilocks” soft landing scenario the place inflation cools to manageable ranges without the economy having to sink into recession.

This comes because the Federal Reserve continues to make use of very tight financial coverage in its ongoing effort to bring inflation down. Whereas it’s true that the Fed has taken a less hawkish tone in 2023 than in 2022, and that the majority economists agree that the ultimate rate of interest hike of the cycle has both already occurred or is close to, inflation nonetheless has to chill extra and stay cool for a little while earlier than the central financial institution is snug with worth stability.

So we should always expect the central bank to keep monetary policy tight, which implies we needs to be ready for tight monetary situations (e.g., greater rates of interest, tighter lending requirements, and decrease inventory valuations) to linger. All this implies monetary policy will be unfriendly to markets in the intervening time, and the chance the economy slips right into a recession can be comparatively elevated.

On the similar time, we additionally know that shares are discounting mechanisms — which means that prices will have bottomed before the Fed signals a major dovish turn in monetary policy.

Additionally, it’s vital to keep in mind that whereas recession dangers could also be elevated, consumers are coming from a very strong financial position. Unemployed individuals are getting jobs, and people with jobs are getting raises.

Equally, business finances are healthy as many firms locked in low interest rates on their debt in recent years. At the same time as the specter of greater debt servicing prices looms, elevated profit margins give firms room to soak up greater prices.

At this level, any downturn is unlikely to turn into economic calamity provided that the financial health of consumers and businesses remains very strong.

And as all the time, long-term traders ought to keep in mind that recessions and bear markets are simply part of the deal whenever you enter the inventory market with the purpose of producing long-term returns. Whereas markets have had a pretty rough couple of years, the long-run outlook for shares remains positive.

Observe: A model of this text was printed on TKer.co.