(Bloomberg) — Bond buyers face the essential determination of simply how a lot threat to absorb Treasuries with 10-year yields on the highest in additional than a decade and the Federal Reserve signaling it’s virtually completed elevating charges.

Most Learn from Bloomberg

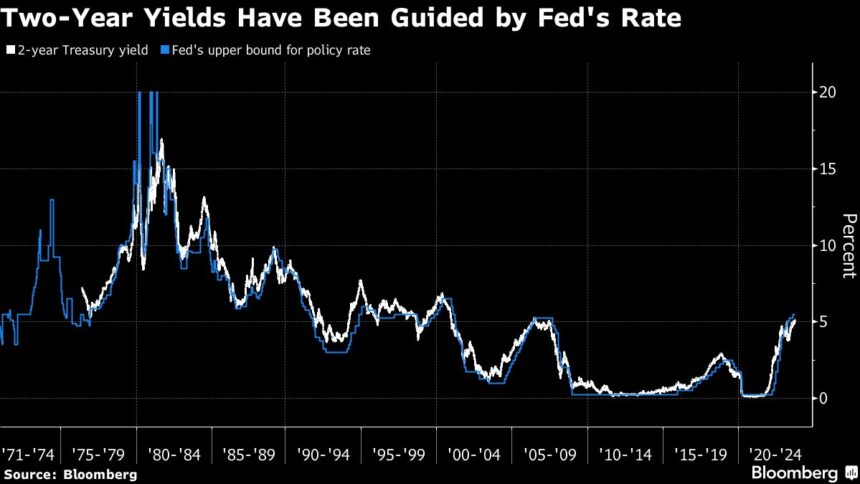

Whereas people are piling into money, for a lot of portfolio managers the controversy now’s about how far to go within the different path. Two-year yields above 5% haven’t been this lofty since 2006, whereas 10-year yields eclipsed 4.5% on Friday for the primary time since 2007.

For Ed Al-Hussainy at Columbia Threadneedle, the candy spot now’s within the shorter-dated notes, which might possible carry out effectively within the occasion the Fed pivots to fee cuts inside a pair years. That maturity additionally avoids the added threat of longer tenors, which have delivered essentially the most ache to bond buyers in 2023 as yields surged broadly amid a resilient financial system and swelling Treasury issuance.

“Until you suppose the Fed’s going to be on maintain for 2 years,” yields above 5% “current fairly good worth,” mentioned Al-Hussainy, a worldwide charges strategist. “The longer finish is the place you get harm essentially the most.”

To increase additional out, he mentioned, “it’s a must to have a stronger view that the labor market goes to crack.” That state of affairs may lead buyers to guess on a recession, spurring a Treasuries rally and fueling outsize features in longer maturities, a operate of their better sensitivity to adjustments in rates of interest.

With the job market proving sturdy, that appears unlikely to occur this 12 months, Al-Hussainy mentioned.

“You may be very affected person earlier than stretching your neck out to get length within the Treasury market,” he mentioned.

Robust Week

Yields rose throughout the curve this week after the Fed saved charges unchanged, whereas penciling in another hike this 12 months and indicating it anticipates retaining borrowing prices elevated effectively into 2024 to tame inflation. It’s an outlook meaning even brief maturities is probably not out of the woods.

What Bloomberg Strategists Say…

“The resounding selloff in front-end Treasuries we now have seen on this cycle isn’t completed but, with yields more likely to attain the best in additional than 20 years ought to the Federal Reserve observe the trail of its newest dot plot.”

– Ven Ram, Markets Dwell strategist

For the total notice, click on right here

Treasuries are down 1.2% this 12 months via Thursday, and are on monitor for an unprecedented third straight annual loss, Bloomberg index information present. Intermediate maturities are roughly flat on the 12 months, whereas longer-dated debt has misplaced 6.6%.

ING Monetary Markets LLC this week mentioned it sees the danger of an extra selloff that drives 10-year yields to five%.

For now, the entrance finish seems to have essentially the most enchantment. For the reason that finish of July, US authorities bond mutual funds and ETFs focusing on maturities of 4 years and fewer have seen round $10.3 billion of inflows, based on EPFR World information via Sept. 20. Center maturities have attracted $3.25 billion, and funds masking past six years have lured $5.5 billion.

Bulls’ Case

For some bond bulls, longer maturities are nonetheless the place to be, regardless of the danger of extra losses. This camp has argued all 12 months that rising borrowing prices are certain to derail development.

Jack McIntyre at Brandywine World Funding Administration mentioned he expects the 4.5% space ought to maintain for the 10-year, given current weak point in equities and rising oil costs.

“Meaningfully decrease fairness valuations would go an extended strategy to tightening monetary circumstances for asset house owners, whereas larger power costs are tightening monetary circumstances for decrease earnings earners,” mentioned the senior portfolio supervisor.

He’s chubby length in rising markets and Treasuries and is looking ahead to proof that the financial system and inflation pressures will cool additional.

It could all be a query of time horizon. For these with lengthier funding mandates, longer-dated Treasuries are at ranges that imply “your start line for future returns is fairly engaging,” mentioned Michael Cudzil, a portfolio supervisor at Pacific Funding Administration Co.

US fiscal deficits and the Fed’s transfer to shrink its steadiness sheet complicate that long-term view. It’s a backdrop that’s prompted buyers to demand a better threat premium on longer-dated debt, serving to steepen the curve from traditionally inverted ranges.

“We’re on this setting the place it’s onerous to check we’re going to return to the extent of long-term charges we had within the final decade,” mentioned Jay Barry, head of US government-bond technique at JPMorgan Chase & Co.

The upshot, he mentioned, is “a steeper yield curve with long-term charges that simply stay elevated even when the market lastly will get snug with the Fed occurring maintain.”

What to Watch

-

Financial information:

-

Sept. 25: Chicago Fed nationwide exercise index; Dallas Fed manufacturing exercise

-

Sept. 26: Philadelphia Fed non-manufacturing exercise; Bloomberg Sept. US financial survey; FHFA home value index; S&P Corelogic US residence value index; new residence gross sales; Convention Board client confidence; Richmond Fed manufacturing index/enterprise circumstances; Dallas Fed providers exercise

-

Sept. 27: MBA mortgage purposes; sturdy items/capital items orders

-

Sept. 28: GDP; preliminary jobless claims; Kansas Metropolis Fed manufacturing exercise; pending residence gross sales

-

Sept. 29: Advance items commerce steadiness; private earnings/spending; PCE deflator; MNI Chicago PMI; U. of Michigan sentiment; Kansas Metropolis Fed providers exercise

-

-

Fed calendar:

-

Sept. 25: Minneapolis Fed President Neel Kashkari

-

Sept. 26: Fed Governor Michelle Bowman

-

Sept. 28: Chicago Fed President Austan Goolsbee; Fed Governor Lisa Prepare dinner; Chair Jerome Powell city corridor with educators; Richmond Fed President Tom Barkin

-

Sept. 29: New York Fed President John Williams

-

-

Public sale calendar:

-

Sept. 25: 13-, 26-week payments

-

Sept. 26: 42-day money administration payments; 2-year notes

-

Sept. 27: 17-week payments; 2-year floating fee notes; 5-year notes

-

Sept. 28: 4-, 8-week payments; 7-year notes

-

Most Learn from Bloomberg Businessweek

©2023 Bloomberg L.P.