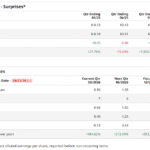

| Contributions to Social Safety Belief Fund (2022) | |

|---|---|

| Supply | Quantity |

| Payroll Tax Contributions | $945.9 billion |

| OASDI Profit Taxes | $47.1 billion |

| Curiosity Earnings | $63.5 billion |

| Normal Fund of the Treasury Reimbursements | $0.2 billion |

| TOTAL | $1,056.7 billion |

Social Safety vs. Non-public Retirement Accounts

People with non-public retirement financial savings accounts have extra management over how a lot and when to contribute than they do with paying Social Safety taxes. For instance, when you work for an organization that gives a 401(ok) plan, you possibly can determine what share of every paycheck (if any) to redirect to that account—though authorities laws place restrictions on how a lot you possibly can contribute.

The annual restrict on 401(ok) contributions is $22,500 in 2023. This quantity will increase to $30,000 if you’re 50 or older, due to the $7,500 catch-up contribution allowed by the federal government. You can not contribute to a Roth IRA in case your adjusted gross earnings (AGI) is $153,000 or increased for singles and $228,000 or increased for married {couples} submitting collectively.

Who Decides What to Pay Out and When?

With a non-public retirement account, corresponding to a 401(ok) or Roth IRA, you determine when to withdraw cash out of your account, and the way a lot to take out. With some retirement accounts, the Inside Income Service (IRS) will make you pay penalties when you take out cash earlier than you attain a sure age or don’t withdraw sufficient cash annually after reaching a sure age. Nonetheless, there’s far more flexibility right here than with Social Safety retirement advantages.

With Social Safety, the federal government decides how a lot to provide you and when. You possibly can determine when to start out receiving advantages, however it might probably’t be till age 62 (the place you accumulate the bottom profit) and age 70 (the place you accumulate the very best profit).

Whilst you cannot change the scale of your Social Safety test, you’re eligible for annual cost-of-living changes (COLAs) that the Social Safety Administration provides beneficiaries annually to take care of their shopping for energy. For 2023, Social Safety and Supplemental Safety Revenue (SSI) advantages elevated by 8.7%. For 2024, the rise is 3.2%.

When you begin claiming advantages, you’ll get a test for a similar quantity each month, based mostly in your lifetime earnings and your age once you began claiming advantages. You possibly can’t determine to withdraw more cash in months when you could have increased bills and fewer cash in months when you could have decrease bills, as you would with an IRA or 401(ok).

If you end up terminally unwell at 40, you possibly can’t declare retirement advantages early based mostly on what you contributed over time. Remember the fact that you might qualify for Social Safety incapacity insurance coverage.

However you possibly can money out your non-public retirement accounts at any time with out getting anybody’s approval, albeit with a penalty in some circumstances. Brokerage companies will not make you show which you could’t work if you wish to take an early withdrawal out of your conventional IRA (although the IRS may if you wish to keep away from penalties by claiming a withdrawal for a medically-related hardship).

Can You Decide-Out of Social Safety?

Few taxpayers can opt-out of paying into the Social Safety system. The Amish, Mennonites, and different non secular teams that rigorously object can typically declare a spiritual exemption from paying into the system so long as in addition they don’t obtain and even qualify to obtain any advantages. If you happen to obtained any advantages, you should still qualify for a spiritual exemption when you repay them.

Individuals who resign their U.S. citizenship might be able to opt-out, relying on their circumstances. Some nonresident aliens don’t must pay into the system, relying on which sort of visa they’ve. Overseas authorities workers based mostly in america and school college students who’re employed by their college are additionally exempt.

What about opting in? Below a public retirement system or a Part 218 settlement, some state and native authorities workers are coated whereas not paying into Social Safety. These workers aren’t allowed to decide into this system.

With non-public retirement financial savings accounts, it’s completely as much as you whether or not to contribute. Even when your employer routinely enrolls you in its 401(ok) plan in an try to nudge you into contributing, you possibly can opt-out if you want.

How Are Social Safety Funds Managed?

The Social Safety system is about up as an intergenerational wealth switch. Which means that all contributions go into one collective pot, so the funds aren’t held in our particular person names. The Social Safety taxes the federal government collects from present staff pay for the advantages of present retirees.

Relying on once you retire, how a lot you earned, and your marital standing, you may even see a greater or worse return by way of getting again roughly than you contributed.

The Risk of Depletion

As a result of completely different generations are completely different in dimension, this construction results in what might be described as timing issues with paying out advantages. Taxes from the immense child boomer era comfortably supported the retirement of the comparatively small Silent Era (born between 1925 and 1945, a lot of these years scarred by the Nice Despair and struggle) and the best era (whose members fought in World Warfare II).

With an increasing number of boomers reaching retirement—and the truth that Era X, the subsequent era, is smaller—it’s estimated that Social Safety’s reserves, additionally referred to as the Previous-Age and Survivors Insurance coverage (OASI) Belief Fund, might be depleted by 2033.

In response to the 2023 annual report from the Social Safety and Medicare Boards of Trustees, the estimated depletion date is 2033. The report additionally cited that the taxes being paid into Social Safety past that 12 months will solely cowl 77% of the scheduled advantages.

Millennials make up an excellent bigger era than the boomers, but it surely’s not clear how properly their monetary contributions will serve to help boomers and Era X, and the way giant future generations can be.

Is a Social Safety Test Socialism?

A Social Safety test just isn’t utterly a socialist program. If it have been a pure socialist program, the quantity that each particular person contributed to it will be the identical and the quantity of the advantages obtained (paid out) by every particular person can be the identical. This isn’t the case.

What Are the Weaknesses of Socialism?

Socialism’s weaknesses embody gradual financial progress, inefficient allocation of assets, low competitors, lack of innovation as a result of low competitors, few alternatives for entrepreneurship, and a scarcity of motivation amongst workers.

What Packages within the U.S. Are Socialist?

Socialist packages and social packages have effective distinctions. Although among the authorities packages within the U.S. may be seen as socialist, they aren’t really socialist. There are, nevertheless, social packages within the U.S., corresponding to Social Safety, Medicare, Medicaid, and the Kids’s Well being Insurance coverage Program.

The Backside Line

The U.S. acquired the thought for a social safety system from Nineteenth-century Germany. That very capitalist monarchy launched an old-age social insurance coverage program in 1889 on the behest of Chancellor Otto von Bismarck, partly to stave off radical socialist concepts being floated on the time. The unique social safety was really an anti-socialist maneuver by a conservative authorities.

Nonetheless, as a result of the American authorities performs such a dominant position within the U.S. Social Safety system—deciding how a lot and when workers and employers pay into the system, how a lot people obtain in advantages once they get them, and stopping nearly everybody from opting out—it solely appears honest to say that Social Safety is, in impact, a type of democratic socialism; nevertheless, it could even be thought of a type of social insurance coverage or a social security internet.

This system requires staff and their employers, together with self-employed people, to pay into the system all through their working years. The federal government controls the cash they contribute and decides when and the way a lot they get again after—and if—they attain retirement age. Having such a profitable and beloved socialist-like program on the coronary heart of such a dedicated capitalistic society is probably the last word paradox. Or possibly it’s simply good frequent sense.