(Bloomberg) — China’s financial system was meant to drive a 3rd of worldwide financial progress this yr, so its dramatic slowdown in current months is sounding alarm bells internationally.

Most Learn from Bloomberg

Policymakers are bracing for a success to their economies as China’s imports of every part from development supplies to electronics slide. Caterpillar Inc. says Chinese language demand for machines used on constructing websites is worse than beforehand thought. U.S. President Joe Biden referred to as the financial issues a “ticking time bomb.”

International buyers have already pulled greater than $10 billion from China’s inventory markets, with many of the promoting in blue chips. Goldman Sachs Group Inc. and Morgan Stanley have minimize their targets for Chinese language equities, with the previous additionally warning of spillover dangers to the remainder of the area.

Asian economies are taking the largest hit to their commerce thus far, together with nations in Africa. Japan reported its first drop in exports in additional than two years in July after China in the reduction of on purchases of vehicles and chips. Central bankers from South Korea and Thailand final week cited China’s weak restoration for downgrades to their progress forecasts.

It’s not all doom-and-gloom, although. China’s slowdown will drag down world oil costs, and deflation within the nation means the costs of products being shipped all over the world are falling. That’s a profit to nations just like the US and UK nonetheless battling excessive inflation.

Some rising markets like India additionally see alternatives, hoping to draw the overseas funding that could be leaving China’s shores.

However because the world’s second-largest financial system, a chronic slowdown in China will harm, relatively than assist, the remainder of the world. An evaluation from the Worldwide Financial Fund exhibits how a lot is at stake: when China’s progress fee rises by 1 share level, world growth is boosted by about 0.3 share factors.

China’s deflation “isn’t such a foul factor” for the worldwide financial system, Peter Berezin, chief world strategist BCA Analysis Inc., mentioned in an interview on Bloomberg TV. “However, if the remainder of the world, the US and Europe, falls into recession, if China stays weak, then that might be an issue — not only for China however for the entire world financial system.”

Right here’s a take a look at how China’s slowdown is rippling throughout economies and monetary markets.

Commerce Droop

Many nations, particularly these in Asia, rely China as their greatest export marketplace for every part from digital components and meals to metals and power.

The worth of Chinese language imports has fallen for 9 of the final 10 months as demand retreats from the file highs set in the course of the pandemic. The worth of shipments from Africa, Asia and North America have been all decrease in July than they have been a yr in the past.

Africa and Asia have been the toughest hit, with the worth of imports down greater than 14% within the first seven months this yr. A part of that is because of a drop in demand for electronics components from South Korea and Taiwan, whereas falling costs of commodities corresponding to fossil fuels are additionally hitting the worth of products shipped to China.

Learn extra: China’s Faltering Development Dangers Derailing Commodities Demand

To date, the precise quantity of commodities corresponding to iron or copper ore despatched to China has held up. But when the slowdown continues, shipments may very well be impacted, which might have an effect on miners in Australia, South America and elsewhere all over the world.

Deflation Strain

Producer costs in China have contracted for the previous 10 months, that means the price of items being shipped from the nation is falling. That’s welcome information for individuals across the globe nonetheless battling excessive inflation.

The value of Chinese language items at US docks has fallen each month this yr and that’s more likely to proceed till manufacturing facility costs in China return to constructive territory. Economists at Wells Fargo & Co. estimate {that a} ‘exhausting touchdown’ in China — which they outline as a 12.5% divergence from its pattern progress — would minimize the baseline forecast for US shopper inflation in 2025 by 0.7 share factors to 1.4%.

Sluggish Tourism Rebound

Chinese language shoppers are spending extra on providers, like journey and tourism, than on items — however they’re not but venturing abroad in giant numbers. Till not too long ago the federal government had banned group excursions to many nations and there’s nonetheless a scarcity of flights, that means it’s way more costly to journey than it was earlier than the pandemic.

Learn extra: China’s Open for Journey However Few Vacationers Are Coming or Going

The pandemic and weak financial system have curbed incomes in China, whereas the years-long housing market hunch means owners really feel much less rich than earlier than. That means it might take a very long time for abroad journey to rebound to the degrees they have been at earlier than the pandemic, hitting tourism-dependent nations in Southeast Asia corresponding to Thailand.

Foreign money Impression

China’s financial woes have pushed the forex down greater than 5% towards the greenback this yr, with the yuan near breaching the 7.3 mark this month. The central financial institution has escalated its protection of the yuan by means of numerous measures together with its day by day forex fixings.

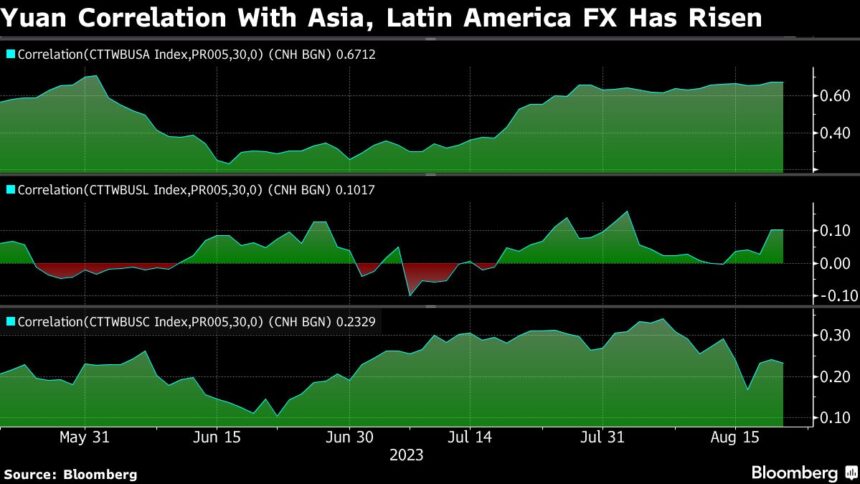

The depreciation within the offshore yuan is having a higher influence on its friends in Asia, Latin America and the Central and Japanese Europe bloc, Bloomberg information present, with the correlation of the Chinese language forex to some others rising.

The weak sentiment spillover could weigh on currencies just like the Singapore greenback, Thai baht, and Mexican peso as correlations rise, in response to Barclays Financial institution Plc.

“With the weaker China financial system it’s very tough to be optimistic on the Asian economies and currencies and we’re extra involved in regards to the metal-exposed currencies,” mentioned Magdalena Polan, head of rising market macro analysis at PGIM Ltd. Weak spot within the development sector might even see currencies of commodity-led economies, such because the Chilean peso and South African rand, endure, she mentioned.

The Australian greenback, which regularly trades as a proxy for China, has misplaced greater than 3% this quarter, the worst performer within the Group-of-10 basket.

Bonds Lose Attraction

China’s rate of interest cuts this yr have lowered the attraction of its bonds to overseas buyers, who’ve minimize their publicity to the market and are in search of alternate options in the remainder of the area.

Abroad holdings of Chinese language sovereign notes are on the lowest share of the overall market since 2019, in response to Bloomberg calculations. International funds had turned extra bullish on the native forex bonds of South Korea and Indonesia as central banks there close to the top of their interest-rate mountain climbing cycles.

Luxurious Shares

Corporations from Nike Inc. to Caterpillar have reported a success to their earnings from China’s slowdown. An MSCI index that tracks world corporations with the largest publicity to China has retreated 9.3% this month, almost double the decline within the broader gauge of world shares.

Learn Extra: International Inventory Managers on Guard as China Ache Set to Unfold

A gauge of European luxurious items and Thailand journey and leisure additionally observe losses to China’s onshore fairness benchmark. The sectors are “correct reflections of how world buyers could take oblique publicity to China and the outlook as China’s financial system continues to weigh,” mentioned Redmond Wong, a market strategist at Saxo Capital Markets in Hong Kong.

Luxurious items corporations corresponding to Louis Vuitton bags-maker LVMH, Gucci-owner Kering SA and Hermes Worldwide are significantly weak to any wobbles in Chinese language demand.

–With help from Marcus Wong and Ernest Tsang.

Most Learn from Bloomberg Businessweek

©2023 Bloomberg L.P.